- Markets @ Midday: Listen here at lunchtime or find all Market Matters Podcasts on Spotify.

The best in six weeks for the ASX today with positive leads from the US and a surprise jump in unemployment reduced rate hike expectations. Oil prices down, bonds yields down and stocks up – hopefully, a sign of things to come.

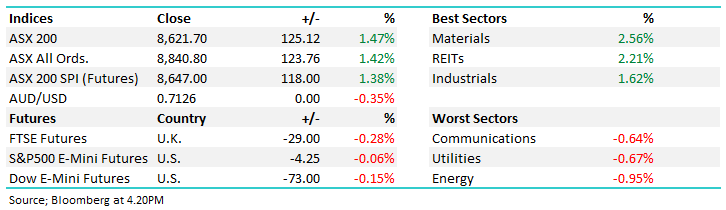

- ASX 200: 8,621.70 / +125.12pts / +1.47% — biggest one-day gain since early April; eight of 11 sectors higher

- AUD/USD: 0.7188 — down on weaker labour market data

- Best sectors: Materials +2.56%, REITs +2.21%, Industrials +1.62%

- Worst sectors: Energy −0.95%, Utilities −0.67%, Communications −0.64%

- Unemployment spiked to 4.5% in April; 18,600 jobs lost vs +15,000 expected. Money markets now pricing just one rate hike this year and only an 11% chance of a move in June (down from 20%).

- ANZ now says the cash rate has likely peaked at 4.35%. NAB pushed its next hike call back to August

- Iran optimism added fuel — Trump said Washington is in the “final stages” of talks with Tehran; Brent crude fell 5.6% to ~$US105-106/bbl; bond yields slid from decade highs.

- Cynics note this looks like a “rinse-and-repeat” Trump jawbone job on oil prices — but the market latched onto it regardless. For what it’s worth, it looks to us like a deal is imminent.

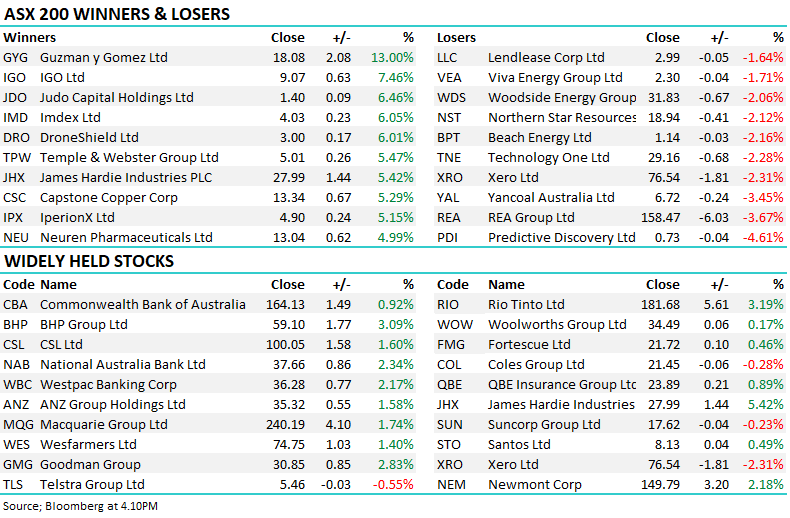

- Gold rebounded toward $US4,550/oz — Newmont (ASX:NEM) +2.18% to $149.79, Evolution Mining (ASX:EVN) +3.78% to close firmer; Northern Star (ASX:NST) −2.12% to $18.94 the exception after MD Stuart Tonkin announced his departure after 13 years — formal succession process now underway

- BHP (ASX:BHP) +3.09% to $59.10 — bounced strongly after four consecutive down days as Materials was the best performing sector

- Rio Tinto (ASX:RIO) +3.19% to $181.68 — also a strong session for the diversified miner

- Banks recovered firmly — Commonwealth Bank (ASX:CBA) +0.92% to $164.13, ANZ (ASX:ANZ) +1.58% to $35.32, Westpac (ASX:WBC) +2.17% to $36.28, NAB (ASX:NAB) +2.34% to $37.66

- James Hardie (ASX:JHX) +5.42% to $27.99 — investors continued to digest full-year results more constructively; Q4 EBITDA beat of $US380.9m. Was up 10% in the US overnight.

- Guzman y Gomez (ASX:GYG) +13.00% to $18.08 — RBC upgraded to Outperform with a $22 price target; analyst flagged the stock is down 26% YTD and the store pipeline is being undervalued by the market

- IGO Limited (ASX:IGO) +7.46% to $9.07 — strong session for the lithium and nickel miner as risk appetite returned to beaten-down resources

- Judo Capital (ASX:JDO) +6.46% to $1.40 — beneficiary of the rate peak narrative; business bank with floating rate loan book. We have this on our Hitlist for the Emerging Companies Portfolio

- Technology One (ASX:TNE) −2.28% to $29.16 — gave back some of yesterday’s post-results gains

- SGH Limited (ASX:SGH) −0.80% lower despite reaffirming FY26 guidance for low-to-mid single digit EBIT growth and leverage below 2x; Crux LNG remains on track for first gas 2H 2027

- Zip Co (ASX:ZIP) +2.73% — secured the right to keep using the Zip brand in Australia after settling trademark dispute with Firstmac

- IperionX (ASX:IPX) +5.15% to $4.90 — commissioned 300-tonne powder metallurgy press at Virginia titanium campus; targeting defence and aerospace demand

- Woodside (ASX:WDS) −2.06% to $31.83, Santos (ASX:STO) +0.49% to $8.13 — energy the worst sector as oil tumbled on Iran optimism; even so prices remain 40%+ above pre-war levels and ADNOC’s CEO warned full supply normalisation won’t occur until well into 2027

- Yancoal (ASX:YAL) −3.45% to $6.72, REA Group (ASX:REA) −3.67% to $158.47 — notable large-cap laggards. We don’t like either, particularly REA given listing volumes will remain under pressure.

- Xero (ASX:XRO) −2.31% to $76.54 — long-duration growth names continued to underperform on the day

- Abacus Group (ASX:ABP) +1.51% after downplaying speculation about a bid.

- GR Engineering (ASX:GNG) secured a $229m EPC contract with Genesis Minerals for the Tower Hill Gold Project in WA

- SkinKandy (ASX:SKK) debuted on the ASX up as much as 7%, last trading +5% at $2.31; raised $160m at $2.20 with market cap of $245.7m

- Iron Ore: $US105.85/mt / −1.3% for the day

- Asian Markets: China −0.9%, Hong Kong –0.5%, Nikkei +3.3%

- Oil: Brent ~US99/bbl — plunged on Iran optimism; Abu Dhabi’s ADNOC CEO warned full supply normalisation won’t occur until well into 2027

- Gold: ~$US4,550/oz — rebounded as bond yields eased

- BoJ watch: Bank of Japan consulting market participants Thursday and Friday on pace of bond purchase tapering as Japanese yields hit multi-year highs — a global spillover risk worth monitoring

- Global Futures: S&P 500 E-Mini −0.06%, Dow E-Mini −0.15%, FTSE −0.28%