- Markets @ Midday: Listen here at lunchtime or find all Market Matters Podcasts on Spotify.

The ASX fell to a seven-week low as bond yields surged to multi-decade highs on war-driven inflation fears, with miners and banks bearing the brunt of a broad global risk-off session. The selling ticked up as the day progressed, and while US Futures also tracked lower for much of it, we failed to embrace a late rally, with the ASX closing near the session lows.

- ASX 200: 8,496.60 / −108.10pts / −1.26% — lowest close since early April; index has now fallen 17 of the last 23 trading days

- AUD/USD: 0.7105 — slumped as the dollar strengthened on rising US yields

- Best sector: Consumer Staples +0.15% — Woolworths (ASX:WOW) +0.64% to $34.43, Coles (ASX:COL) +0.47% to $21.51; defensive income the only hiding place

- Worst sector: Materials −2.12% — gold stocks hammered as rising US yields and a stronger USD eroded the precious metal’s investment case

- Bond markets the central story — US 30-year yield hit 5.20% (highest since 2007), AU 10-year at 5.10%, AU 15-year at 5.29% (highest since 2011); money markets now pricing 81% chance of a Fed rate hike this year

- Gold under pressure — fell toward $US4,466/oz; Newmont (ASX:NEM) −4.46% to $146.59, Evolution Mining (ASX:EVN) −4.85% to $11.37, Greatland Resources (ASX:GGP) −6.25% to $12.30

- BHP Group (ASX:BHP) −2.33% to $57.33 — fourth consecutive down day; iron ore below $US107/t as Chinese steel demand deteriorates (new construction starts −27% YoY in April, worsening from −17% in March)

- Banks dragged lower — Morgan Stanley warned operating conditions for the big four are changing at the fastest pace in 25 years outside COVID; Westpac (ASX:WBC) −2.42% to $35.51, ANZ (ASX:ANZ) −2.11% to $34.77, NAB (ASX:NAB) −0.65% to $36.80, Commonwealth Bank (ASX:CBA) −0.15% to $162.64

- Commonwealth Bank (ASX:CBA) flagged a “dangerous minefield” — Iran conflict, sticky inflation and budget housing changes the three key risks; warned oil could hit $US150/bbl if the Strait of Hormuz remains closed, which could reduce house prices ~3% over three years

- Energy the relative bright spot — oil holding ~$US111/bbl; Woodside (ASX:WDS) −0.68% to $32.50, Santos (ASX:STO) flat at $8.09

- Technology One (ASX:TNE) +7.34% to $29.84 — best on market after Barrenjoey upgraded to Overweight post results yesterday

- Tuas (ASX:TUA) −16.85% to $2.22 — third straight double-digit move after Singapore’s regulator flagged potential spectrum law breach; extraordinary volatility continues

- Webjet (ASX:WEB) −6.30% to $2.23 — record low close after Virgin Australia cut commissions; bookings, EPS and profit all going backwards; sitting duck for Helloworld (18.3% stake) or BGH Capital (13.3%)

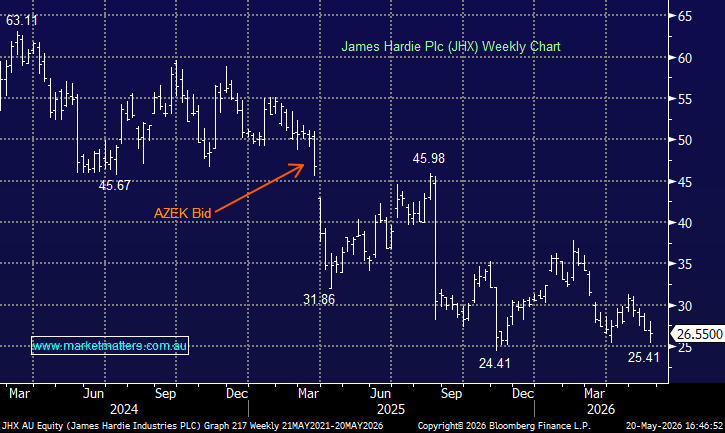

- James Hardie (ASX:JHX) −0.86% to $26.55 — Q4 EBITDA beat at $US380.9m, but FY27 guidance ~1.8% below consensus; management “not assuming a market recovery”; single-family construction assumed −5%, R&R −2%

- Catapult (ASX:CAT) +17.7% to $3.39 — management EBITDA +67% YoY to $US24.7m; standout result in a sea of red

- Electro Optic Systems (ASX:EOS) −10.3% to $7.91 — $150m institutional raise at $8/share plus $40m strategic placement from defence investors

- Brambles (ASX:BXB) −6.45% to $16.40 — notable large-cap loser on the day

- Goodman Group (ASX:GMG) −2.12% to $30.00, Macquarie (ASX:MQG) −2.03% to $236.09, Wesfarmers (ASX:WES) +1.01% to $73.72

- Wages data — ABS: total wages and salaries hit a record $110.6bn in March, +6% YoY; WA led with mining bonuses driving +8.4% sector growth

- Consumer spending — NAB data showed stabilisation through May 9; travel remains the weakest discretionary category with elevated air travel refund activity

- Oil: trading around $US111/barrel (WTI)

- Gold: traded down ~$US15/oz to around $US4,466/oz at our close

- Iron Ore: $US107/mt / −0.8% for the day

- Asian Markets: China −0.5%, Hong Kong −1.6%, Nikkei −1.9%

- Global Futures: S&P 500 E-Mini −0.66%, Dow E-Mini −0.73%, FTSE −1.07% (at time of writing)