- Markets @ Midday: Listen here at lunchtime or find all Market Matters Podcasts on Spotify.

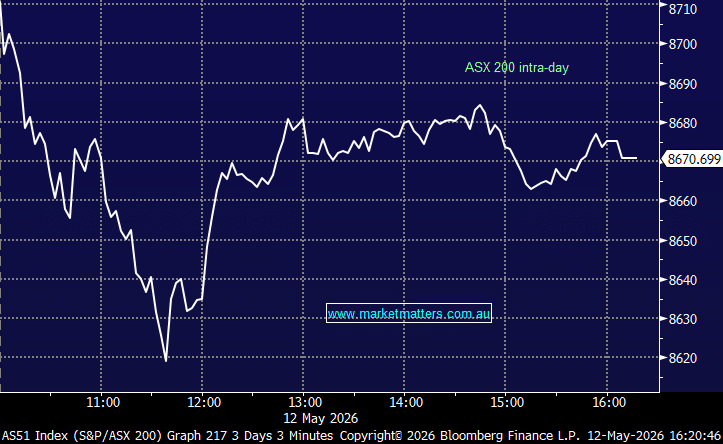

The ASX was weaker today, with the market unable to follow a stronger offshore lead as investors turned more cautious ahead of tonight’s Federal Budget. Lots of leaks in recent days and suffice to say, this will be one of the more important budgets in recent memory with the ALP fiddling with capital gains tax.

Weakness was fairly broad-based today, though the index was cushioned by a strong session from the miners after copper pushed to record highs. We covered our view on Copper and related stocks this morning Here.

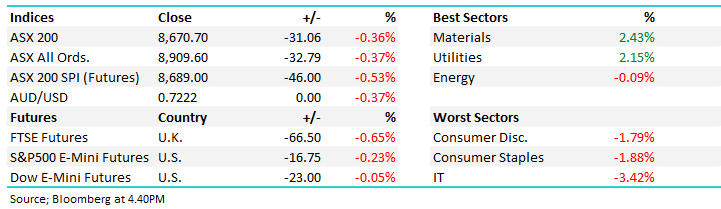

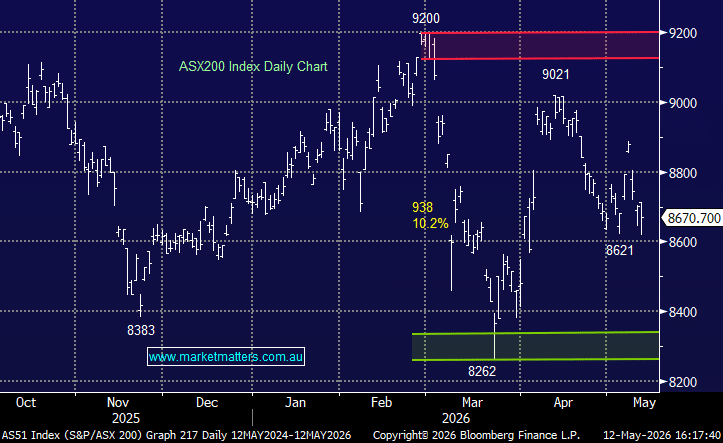

- ASX 200: 8,670.70 / −31.06pts / −0.36%

- AUD/USD: 0.7222 / -0.46%

- Best sectors: Materials +2.43%, Utilities +2.15%, Energy -0.09%

- Worst sectors: Consumer Disc. −1.79%, Consumer Staples −1.88%, IT −3.42%

- Pressure was most obvious in Technology, where WiseTech (WTC) -5.87%, Xero (XRO) -3.52% and Life360 (360) -10.89% all came under pressure. Life360 was hit after downgrading user growth guidance, blaming a technical issue that suppressed new users, with the company not expecting a full recovery until the third quarter – more on this tomorrow morning.

- Healthcare remained under pressure, with CSL (CSL) -2.18% adding to yesterday’s 16% fall after its latest downgrade triggered a wave of broker cuts from Citi, RBC, Jarden and Canaccord. ResMed (RMD) -3.35% and Cochlear (COH) -0.01% also weighed on the sector.

- The banks were softer, with Westpac (WBC) -1.37%, CBA (CBA) -1.40%, ANZ (ANZ) -2.12% and NAB (NAB) -2.09% all lower. The local market continues to struggle with the mix of higher domestic rates, slowing activity and uncertainty around tonight’s Budget.

- Materials was the standout, rising +2.43%, helped by copper closing at a record high. BHP (BHP) +2.49% hit a record (above $60) and overtook CBA as the ASX’s largest company by market capitalisation, while Rio Tinto (RIO) +3.13% and South32 (S32) +3.57% also rallied.

- Energy also held up, with Brent crude adding +0.9% to US$105.15/bbl as President Trump raised doubts over a ceasefire with Iran. Woodside (WDS) +0.75% and Santos (STO) +0.53% were firmer.

- DroneShield (DRO) -9.92% was hit after confirming ASIC had launched an investigation into ASX disclosures made in November 2025 and trading in the company’s shares around the same period. The issue follows earlier incorrect sales information and large share sales by the former CEO, chairman and another director.

- IAG (IAG) +1.91% edged higher after outlining its refreshed “Ambition 2030” strategy, targeting more than $25bn in gross written premium and 11m+ customers by 2030. The market took the update reasonably well, though we would still frame this as incremental rather than a major near-term catalyst.

- Steadfast (SDF) -2.21% fell after announcing a minimum holding buy-back for small shareholders with holdings worth less than $500, while BWP Group (BWP) -1.06% slipped as it launched a $106m retail raising at $3.77/share as part of its broader $228m entitlement offer.

- Centuria Industrial (CIP) +0.68% reaffirmed FY distribution guidance at 16.8c from earnings of 18.2-18.5c. They divested 4 properties for $188m at an average premium to book value of 17% – a good outcome. The current yield based on guidance is 5.65%.

- NAB’s business survey showed conditions falling for a fourth straight month in April, with purchase cost growth accelerating sharply and margin pressure building across manufacturing and construction. This supports the view that the energy shock is increasingly biting at the business level, even as demand softens.

- Business credit demand was also soft, with Equifax reporting overall demand down -0.4% in the March quarter. The more concerning element was the divergence between stable borrowers and higher-risk SMEs, with Equifax noting high-risk small businesses appear to be “accelerated credit shopping”.

- Oil: trading around $US99.22 (WTI) +1%

- Gold: trading around $US4706/oz around our close, -0.61% on the day

- Iron Ore: $110.80/mt / -0.7% for the day

- Asian Markets: China -0.50%, Hong Kong +0.1% and the Nikkei +0.63%.

- Global Futures: S&P 500 E-Mini −0.23%, Dow E-Mini −0.05%, FTSE −0.65%

- US Earnings Tonight: JD.com (JD US)