- Markets @ Midday: Listen here at lunchtime or find all Market Matters Podcasts on Spotify.

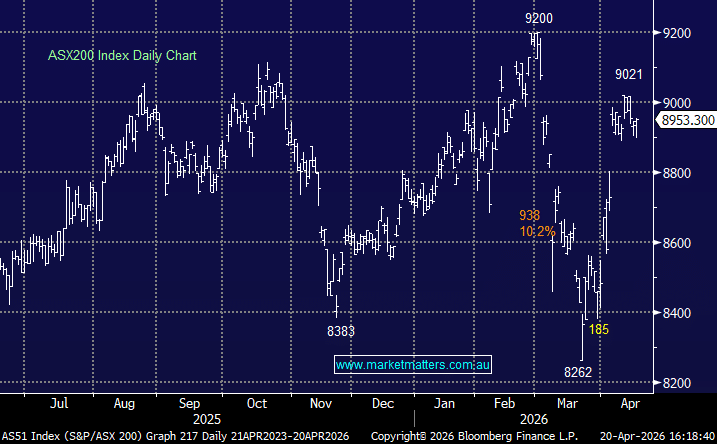

SPI Futures were pricing a rise today of +82pts following strength in the US on Friday night, however the weekend news flow was anything but positive, with the Strait of Hormuz closing just as quickly as it opened. Oil prices spiked ~8% first up this morning, Gold fell ~$US40, US Futures traded down ~0.7% and Australian equities opened flat – which is where they closed – not a bad effort considering.

While macro headlines continue to drive sentiment, the session ultimately evolved into a fairly balanced one under the surface. Banks and large resource names weighed, but strength in discretionary, technology and property stocks helped steady the market as the day progressed.

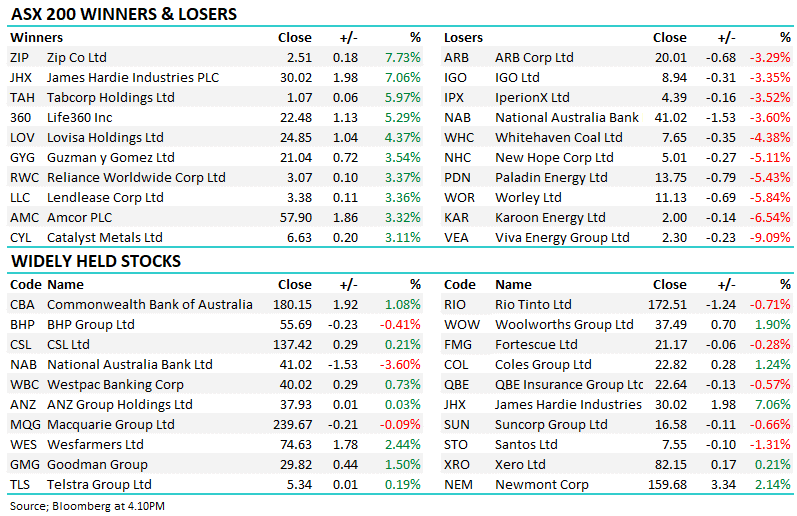

- ASX 200: 8,953.30 / +6.37pts / +0.07%

- AUD/USD: 0.7145 / −0.40%

- Best sectors: Consumer Disc. +1.52%, Consumer Staples +1.37%, REITs +1.06%

- Worst sectors: Financials −0.10%, Utilities −0.84%, Energy −3.00%

- Financials were mixed — National Australia Bank (ASX: NAB) −3.60% fell after flagging a sharp increase in credit impairment charges tied to macro uncertainty, while Commonwealth Bank (ASX: CBA) +1.08% and Westpac (ASX: WBC) +0.73% traded higher.

- Gold miners found support as the gold price recovered from early losses, with Ora Banda Mining (ASX: OBM) +4.7%, Vault Minerals (ASX: VAU) +1.73%, Regis Resources (ASX: RRL) +1.72% and Evolution Mining (ASX: EVN) +1.77% all moving higher through the session.

- Lithium, uranium and energy stocks were weaker, with some profit taking emerging after the sector’s strong run in recent weeks – Mineral Resources (ASX: MIN) −2.03%, Paladin Energy (ASX: PDN) −5.43%, Deep Yellow (ASX: DYL) −2.96% and IGO (ASX: IGO) −3.35% all traded lower.

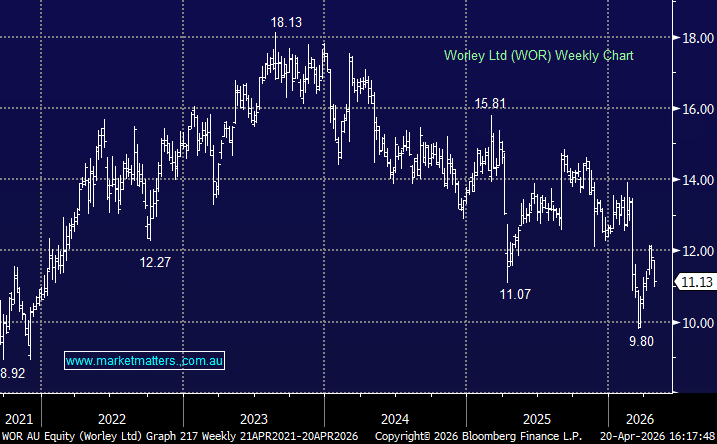

- WOR –5.84% flagged a hit to FY26 earnings from the Middle East conflict, with project delays now expected to reduce underlying EBITA by $30–40 million.

- Zip Co (ASX: ZIP) +7.73% continued to rally following last week’s strong quarterly update, with investors encouraged by improving US growth.

- NextDC (ASX: NXT) went into a trading halt, announcing a $1.5bn equity raising to accelerate its data centre expansion plans.

- Worley (ASX: WOR) −5.84% slipped after warning that disruption from the Middle East conflict could reduce FY26 underlying EBITA by around $30–40 million due to delays in project awards.

- Viva Energy (ASX: VEA) −9.09% came out of a trading halt this morning after the fire at its Geelong refinery last week with gasoline production now running at ~60% of normal capacity.

- 4DMedical (ASX: 4DX) −2.57% was weaker after announcing a new contract with GlaxoSmithKline to supply lung imaging analytics for pulmonary drug development.

- Oil: Trading around $US90.55/barrel (WTI)

- Gold: Was down -0.9% trading at $US4,788/oz around our close.

- Iron Ore: Up +0.64% to $US106.36/mt

- Asian Markets: China +0.56%, Hong Kong +0.64% and the Nikkei +0.20%.

- Global Futures: S&P 500 E-Mini −0.63%, Dow E-Mini −0.72%, FTSE −0.38%