- Markets @ Midday: Listen here at lunchtime or find all Market Matters Podcasts on Spotify.

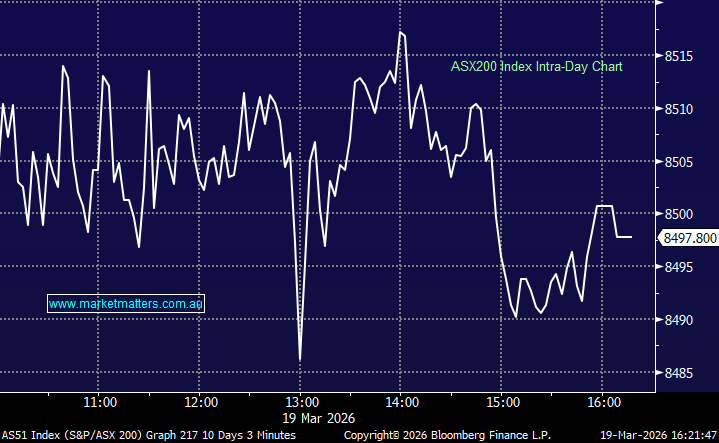

The ASX 200 fell sharply today, the damage felt heavily in the resources with gold miners hit hardest as bullion dropped overnight on stronger USD following the Fed’s interest rate hold, while rate-sensitive growth and property stocks continued to struggle in the higher-for-longer rate environment. Energy was the obvious standout, surging more than 5% as oil pushed higher. Employment data offered a lift early in the session as the Aussie dollar and yields softened on shifting rate expectations for the May RBA meeting, though this was short lived and most of the damage was done on the open, with the market ultimately trading around the 8500 level for most of the day.

- ASX 200: 8,497 / −142pts / −1.65%

- AUD/USD: 0.7041 / flat / +0.26%

- Best sectors: Energy +5.08%, Consumer Staples +0.91%, Utilities +0.36%

- Worst sectors: Materials −4.83%, IT −2.97%, REITs −2.37%

- Australia’s labour market delivered mixed signals as we saw February jobs data at 11:30am, with the unemployment rate rising to 4.3% vs 4.1% survey expectation. The participation rate increased with 48,900 jobs added in February, well above expectations of around 20,000 though largely driven by an increase in part-time and the participation rate. May rate hike odds came back from 73% to 57% off the back of the data.

- Viva Energy (VEA) +15.17% was the standout performer of the entire session — a massive move that reflected the sharp surge in oil prices and the leverage smaller energy names carry in this environment.

- Woodside Energy (WDS) +7.19% was the most significant large-cap energy mover with the company also appointing former Anglo-American CEO Mark Cutifani as a new director.

- Yancoal (YAL) +8.54%, New Hope (NHC) +5.33% and Whitehaven Coal (WHC) +2.29% all gained as tightening energy supply continued to drive energy-switching bets into thermal coal.

- Santos (STO) +3.22%, Ampol (ALD) +4.60% and Karoon Energy (KAR) +5.51% all participated in the energy rally.

- Worley (WOR) +2.95% also firmed with the engineering services group standing to benefit from elevated capex spending in the energy sector in a higher oil price environment.

- Gold miners were the session’s clear disaster zone. Northern Star (NST) −9.50% Evolution Mining (EVN) −9.56% and Genesis Minerals (GMD) −10.70% hit hard as bullion dropped sharply overnight.

- WiseTech Global (WTC) −7.02% was the worst performer in the technology sector as higher-for-longer rate fears continued to hammer duration-sensitive growth names. Xero (XRO) −3.04% also slid, extending the tech sector’s recent slide.

- BHP (BHP) −3.47%, Rio Tinto (RIO) −3.22% and Fortescue (FMG) −3.35% all fell heavily as the materials sector bore the brunt of the day’s selling alongside gold.

- The property sector also gave ground, with Scentre Group (SCG) −3.06%, Mirvac (MGR) −2.96% and Lendlease (LLC) −3.45% all lower.

- Lynas Rare Earths (LYC) −2.06% slipped on broader sentiment, though announced the first production of samarium oxide at its Malaysian facility, diversifying its product rare earths product mix.

- Boss Energy (BOE) −6.75% fell even after reporting an increase in uranium resources at its South Australian satellite deposits – a case of good news drowned out by macro tape.

- PLS Group (PLS) −10.02% and Liontown Resources (LTR) −6.77% were among the lithium names lower on the session.

- Oil traded steady $US110/bbl after surging overnight.

- Iron Ore traded up slightly at $107.50/mt.

- Gold rose slightly to around $US4,840/oz at our close.

- Futures: S&P 500 E-Mini −0.05%, Dow E-Mini −0.02%, FTSE −0.97%.