- Markets @ Midday: Listen here at lunchtime or find all Market Matters Podcasts on Spotify.

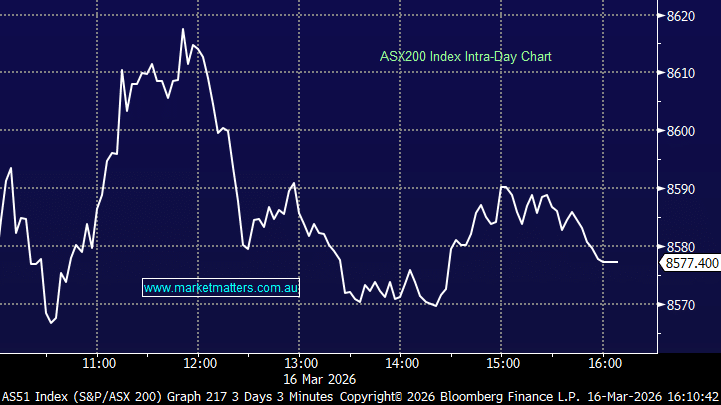

The ASX 200 fell as a broad sell-off in the mining sector overwhelmed a solid showing from defensives and financials. Six of eleven sectors finished higher, but that didn’t matter much when the heavyweights were doing the damage. Gold miners were hit as bullion continued to slide following two consecutive weeks of declines. Iron ore stocks also weighed after China’s state-backed trader eased restrictions on BHP ore grades — partially unwinding last week’s fear-driven rally as fresh data showed Chinese steel output fell 3.6% in the first two months of the year.

All of this played out right as we approach the RBA’s rate decision tomorrow. The market is almost fully priced for a hike which kept a lid on any recovery attempts, and while US futures are pointing higher tonight, the domestic mood remains cautious.

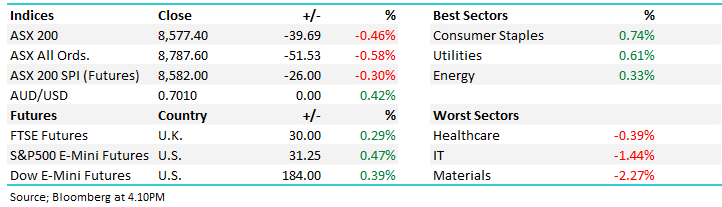

- ASX 200: 8,577.40 / −39.69pts / −0.46%

- AUD/USD: 0.7010 / flat / +0.42%

- Best sectors: Consumer Staples +0.74%, Utilities +0.61%, Energy +0.33%

- Worst sectors: Healthcare −0.39%, IT −1.44%, Materials −2.27%

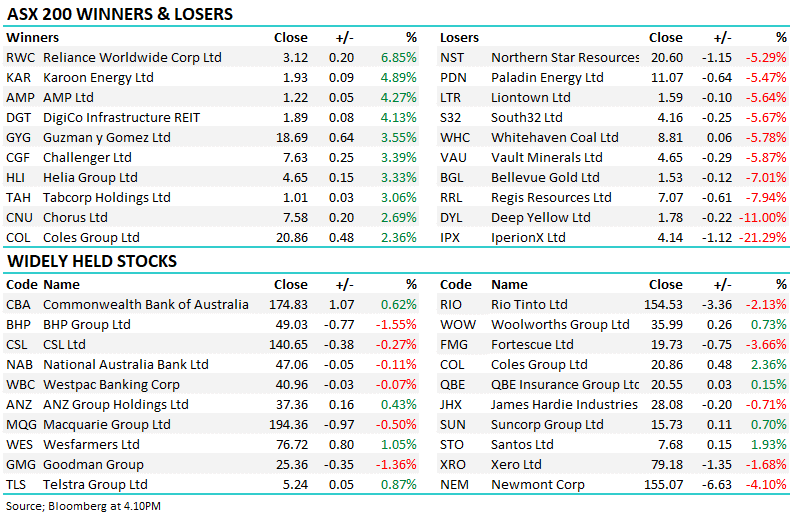

- Gold miners were the session’s standout victims as Newmont (NEM) −4.10% and Regis Resources (RRL) −7.94% headed up the biggest losers in the sector.

- Iron ore and diversified miners retreated sharply as Fortescue (FMG) −3.66%, Rio Tinto (RIO) −2.13% and BHP (BHP) −1.55% fell on softer commodity prices.

- South32 (S32) −5.67% placed its Mozal aluminium smelter in Mozambique on care and maintenance, flagging one-off costs of $US60 million and ongoing annual costs of $US5 million.

- Reliance Worldwide (RWC) +6.85% signalled underlying business strength as it announced a further $120 million on-market share buyback.

- Energy stocks were well supported with Woodside (WDS) +1.61%, Santos (STO) +1.93% following brent crude prices higher.

- Guzman y Gomez (GYG) +3.55% gained despite news of co-CEO Hilton Brett stepping back to undergo surgery.

- Perpetual (PPT) +2.19% rose on news it has agreed to sell its wealth management business to Bain Capital for $500 million upfront, with potential earn-out payments of up to $50 million.

- Lynas Rare Earths (LYC) +1.55% climbed after signing a binding letter of intent with the US Department of Defence to supply rare earth oxides, with $US96 million allocated over four years.

- The banks were mixed and largely treading water ahead of tomorrow’s RBA decision. CBA +0.62% and ANZ +0.43% firmed modestly, while Westpac (WBC) −0.07% and NAB −0.11% were barely changed. The rate move is all but priced in — the question now is whether the board signals a pause or opens the door to a further hike in May.

- IperionX (IPX) −21.29% was the worst performer on the index after saying it was unaware of the reason for the price drop – the fall centered around the mechanics of its US Department of Defence grants with spending upfront before reimbursement.

- Oil held around $US99.50/barrel.

- Gold was under pressure early but held to above $5,000/oz to close the session.

- Asian markets: China –0.3%, Hong Kong +1.3% and the Nikkei –0.2%.

- Global Futures: FTSE +0.29%, S&P 500 E-Mini +0.47%, Dow E-Mini +0.39%.