- Markets @ Midday: Listen here at lunchtime or find all Market Matters Podcasts on Spotify

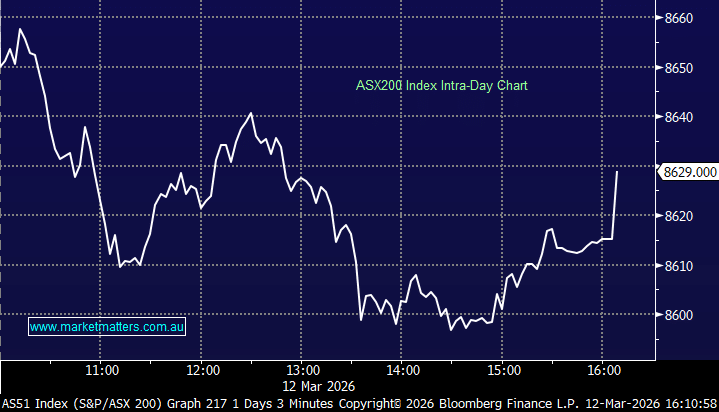

The ASX 200 was hit today inline with a sell-off in US Futures during our time zone as an escalation in the Middle East sent oil prices back above $US100 following attacks on two oil tankers in Iraqi waters, combined with Oman clearing all vessels from its Mina Al Fahal export terminal. Iraq suspended operations at all its oil ports, overshadowing the overnight announcement by the IEA around a record release of strategic reserves.

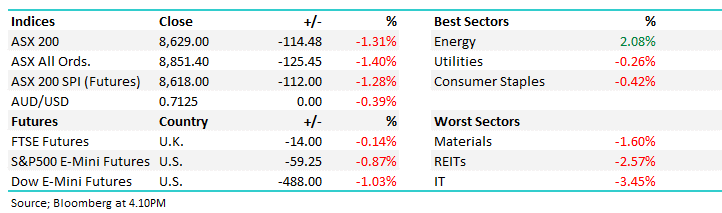

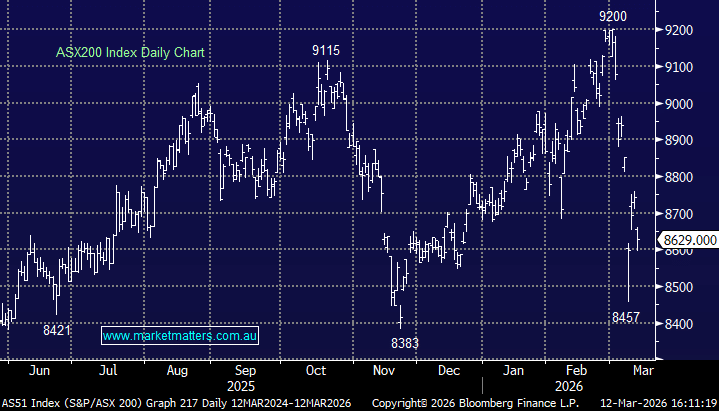

- ASX 200: 8,629 / −114.48pts / −1.31%

- AUD/USD: 0.7125 / −0.39%

- Best sectors: Energy +2.08%, Utilities −0.26%, Consumer Staples −0.42%

- Worst sectors: Materials −1.60%, REITs −2.57%, IT −3.45%

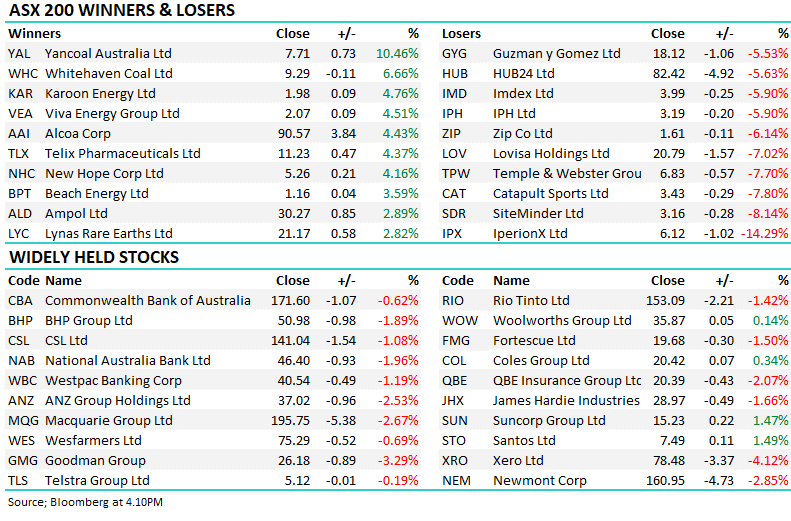

- Energy was the only sector to rally. Yancoal (YAL) +10.5% to $7.71 — a 52-week high — and Whitehaven Coal (WHC) +6.7% to $9.29 led the charge as coal prices surged alongside oil. UBS upgraded its sector forecasts.

- Karoon Energy (KAR) +4.8% to $1.98, Ampol (ALD) +2.9% to $30.27, and Woodside (WDS) +2.1% to $31.05 all participated. Alcoa (AAI) +4.4% to $90.57 after UBS upgraded aluminium forecasts tied to the Middle East situation and named it as its preferred Australian exposure, lifting its price target to $95.

- IT and growth were the session’s clear casualties as bond yields stayed elevated. Xero (XRO) −4.1% to $78.48 and WiseTech Global (WTC) −2.6% to $47.96 both copped selling.

- Real estate was weak. Goodman Group (GMG) −3.3% to $26.18 and Scentre Group (SCG) −1.4% to $3.49. REITs were the second-worst sector on the day, reflecting ongoing sensitivity to the higher-for-longer rate narrative.

- Materials gave back Wednesday’s strong gains. BHP (BHP) −1.9% to $50.98, Rio Tinto (RIO) −1.4% to $153.09 and Newmont (NEM) −2.9% to $160.95.

- Iron ore and base metals couldn’t hold onto the prior session’s momentum in the face of broader risk aversion.

- Banks were broadly weaker despite being rate-rise beneficiaries in theory. ANZ −2.5% to $37.02 and NAB −2.0% to $46.40 led losses.

- Oil’s move was the key, with ANZ’s commodity strategist Daniel Hynes saying the market is underestimating the risk that early logistical disruptions evolve into sustained production losses — describing it as an “attrition phase.”

- The bank has lifted its end-of-June Brent forecast to $US100/bbl, cautioning that emergency reserves are “a bridge, not a substitute, for lost production.”

- Australian household spending fell for the first time since September 2024, according to the CBA Household Spending Insights Index, which declined 0.5% in February after 17 consecutive months of growth.

- Annual growth slowed to 4.9% — the weakest since August 2025. Utilities fell the most sharply (−6.4%), with education and discretionary categories also softening.

- Ora Banda Mining (OBM) +1.4% to $1.43: New drilling expanded the high-grade Little Gem gold prospect in WA, uncovering a previously unknown mineralised zone called the Sapphire Trend. A solid follow-through from yesterday’s explosive +21% session on the Round Dam resource upgrade.

- Collins Foods (CKF) +5.2% to $9.92: Agreed to acquire eight KFC restaurants in Bavaria, expanding its German footprint in a market it has identified as a key growth opportunity.

- Alcoa (AAI) +4.4% to $90.57: UBS upgraded its aluminium price forecasts citing the Middle East situation and named Alcoa as its preferred Australian exposure, lifting its price target to $95.

- IperionX (IPX) −14.3% to $6.12: Net losses doubled over the December half to $US34.8 million as R&D and exploration costs accelerated. The worst performer in the ASX 200 today — the market is losing patience with the path to commercialisation.

- Liontown Resources (LTR) −0.9% to $1.61: Reported a net loss of $184 million for the half year to December 31, driven by a $104.4 million non-cash charge linked to a convertible note held by LG Energy Solution. Revenue more than doubled but the headline number dominated.

- Atlas Arteria (ALX) −1.3% to $4.51: Fell despite positive news out of Virginia, where the legislature passed a bill extending toll increase approval windows from one to two years.

- Gold was down $US24/oz at $US5,150/oz

- Asian Markets were lower: Hong Kong -1.2%, Japan -1.8% and China -0.4%

- Futures: S&P 500 E-Mini −0.87%, Dow E-Mini −1.03%, FTSE −0.14%