- Markets @ Midday: Listen here at lunchtime or find all Market Matters Podcasts on Spotify

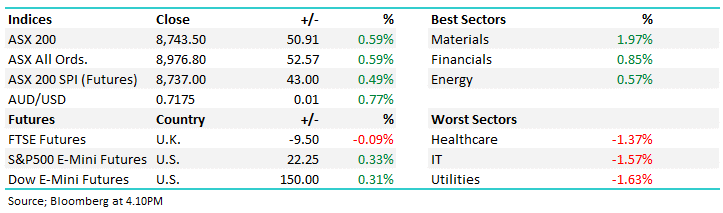

The ASX pushed higher on Wednesday, closing up 0.6% as miners and banks did the heavy lifting in a session defined almost entirely by a hawkish pivot from the RBA. It wasn’t a broad rally — only four of eleven sectors finished in the green — but the heavyweights were enough to keep the index comfortably in positive territory. Overnight US futures are pointing to a modestly positive Wall Street open.

The dominant theme was monetary policy. RBA deputy governor Andrew Hauser warned that failing to act decisively on inflation could allow price expectations to become “toxic.” Money markets moved sharply, lifting the probability of a rate rise at next week’s March 17 meeting to 77%, up from 38% before his remarks. NAB, Westpac, UBS, Deutsche Bank and Citi all brought forward their rate rise calls to next week, with several pencilling in a follow-up hike in May for a terminal rate of around 4.35%. The Australian dollar surged to US71.75¢, its highest in more than three years.

We were of the view that the RBA should wait on April’s CPI print and May’s Federal Budget, but Hauser’s comments we think pretty much seals the deal for a move next week, with future tightening resting on the upcoming data.

- ASX 200: 8,743.50 / +50.91pts / +0.59%

- AUD/USD: 0.7175 / +0.77%

- Best sectors: Materials +1.97%, Financials +0.85%, Energy +0.57%

- Worst sectors: Healthcare -1.37%, IT -1.57%, Utilities -1.63%

- The rate rise repricing drove a sharp rotation out of growth and rate-sensitive names, into banks and hard assets. Bond yields climbed and the AUD surged, with 10-year Aussie bonds auctioned at a weighted average yield of 4.90%.

- Banks were the obvious beneficiary. ANZ (ANZ) +1.82% to $37.98 led the sector, with NAB (NAB) +1.05% to $47.33, CBA (CBA) +0.51% to $172.67 and Westpac (WBC) +0.47% to $41.03 all firming. Macquarie Group (MQG) added 1.31% to $201.13.

- Lynas Rare Earths (LYC) was the ASX 200’s best performer, up 16.2% to $20.59 after locking in a long-term supply deal with Japan Australia Rare Earths through to 2038 — a significant offtake agreement for critical minerals. Hard to chase at these levels but the strategic logic is sound. Other Rare Earth stocks joined the party. Iluka Resources (ILU) +9.36% to $6.66

- Champion Iron (CIA) +6.93% to $4.94 had strong sessions as iron ore climbed back above $US104 a tonne

- Ora Banda Mining (OBM) rocketed over 21% after announcing a near-tenfold expansion of its Round Dam gold resource to 1.33 million ounces, lifting its total global resource base by 57% to 3.3 million ounces.

- Fortescue (FMG) +3.68% to $19.98 and BHP (BHP) +1.42% to $51.96 as the materials sector led the index.

- Northern Star (NST) +3.04% to $26.75 and Newmont (NEM) +1.64% to $165.68 both rallied with bullion.

- DroneShield (DRO) +1.49% to $4.08 after announcing EU counter-drone manufacturing, with delivery of European-made systems scheduled for mid-2026 and total production capacity targeted to grow to $2.4 billion by end of year.

- Macquarie Technology Group (MAQ) +7% after securing a $200 million hybrid investment from the National Reconstruction Fund Corporation for sovereign digital infrastructure expansion.

- WiseTech Global (WTC) -3.60% to $49.24, Xero (XRO) -2.23% to $81.85 and Goodman Group (GMG) -1.49% to $27.07 all copped selling as the rate repricing hit growth and real estate names hard. JB Hi-Fi (JBH) -1.50% to $78.71 and CSL -1.37% to $142.58 also gave ground.

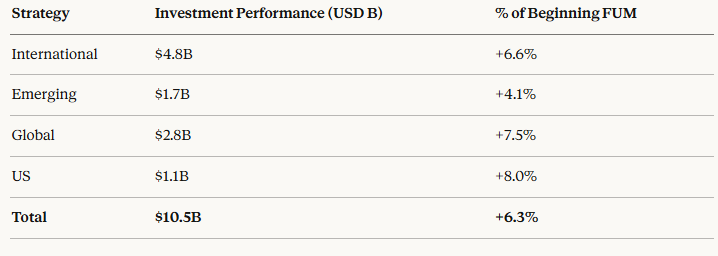

- GQG Partners (GQG) -5.50% to $1.80 despite FUM rising to $US172.9 billion. The market fixated on $US3.2 billion in net outflows for February, which overshadowed an impressive $US10.5 billion investment performance gain for the month. At current levels this looks like an overreaction to us — the underlying performance numbers were strong.

- AGL Energy (AGL) -5.55% to $9.02 was among the day’s worst performers on a Macquarie downgrade from buy equivalent to hold ($9.61 PT)

- Centuria Capital (CNI) -5.73% to $1.65 also had a tough session having looked like it had found a floor early – disappointing afternoon session.

- Oil eased to around $US86.93/barrel (-1%) after the WSJ reported the IEA is proposing a record release of strategic reserves exceeding the 182 million barrels deployed in 2022.

- Woodside (WDS) +0.80%, Santos (STO) +0.14% and Ampol (ALD) -1.70%.

- Bitcoin rallied close to 6% on the week to trade around $US70,000, supported by $US1.52 billion in ETF inflows over three weeks.

- Gold pushed above $US5,200/oz

- Asian markets are mixed: Hong Kong -0.3%, Japan +1.5% and China +0.1%

- Futures: S&P 500 E-Mini +0.33%, Dow E-Mini +0.31%, FTSE Futures -0.09%