- Markets @ Midday: Listen here at lunchtime or find all Market Matters Podcasts on Spotify

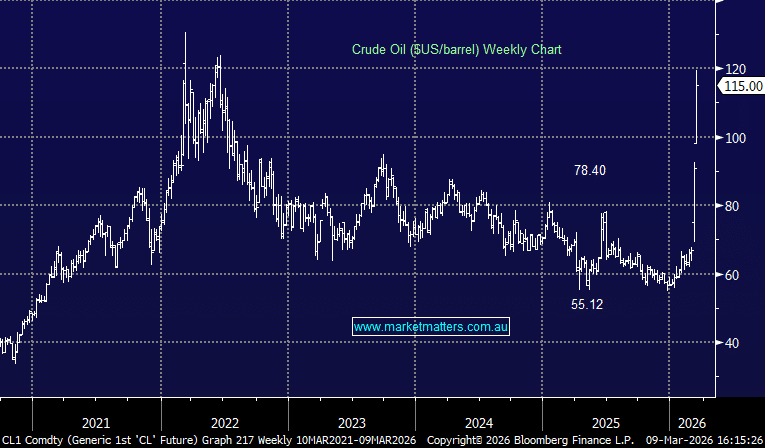

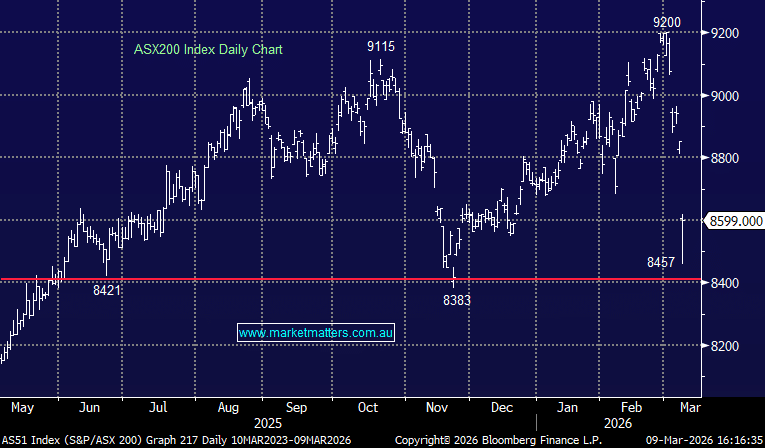

A brutal start to the week with the ASX experiencing its worst session since Liberation Day in April last year and the steepest intraday fall since the COVID crash of 2020. The move was driven by a ~25% spike in Oil prices this morning that triggered an indiscriminate sell-off across the region in both stocks and bonds, with yields moving materially higher throughout the session.

The Strait of Hormuz has been effectively shut for nine days, the UAE and Kuwait are curbing production, Qatar has warned that all Persian Gulf gas output could cease within days, and Iran, having just named a new supreme leader, has signalled capacity for months of sustained conflict. Oil surging ~25% in a session is not a normal event, and markets are repricing accordingly. Inflation expectations are ripping, bond markets are selling off hard, and central bank rate hike bets are back on the table in a way we haven’t seen in years.

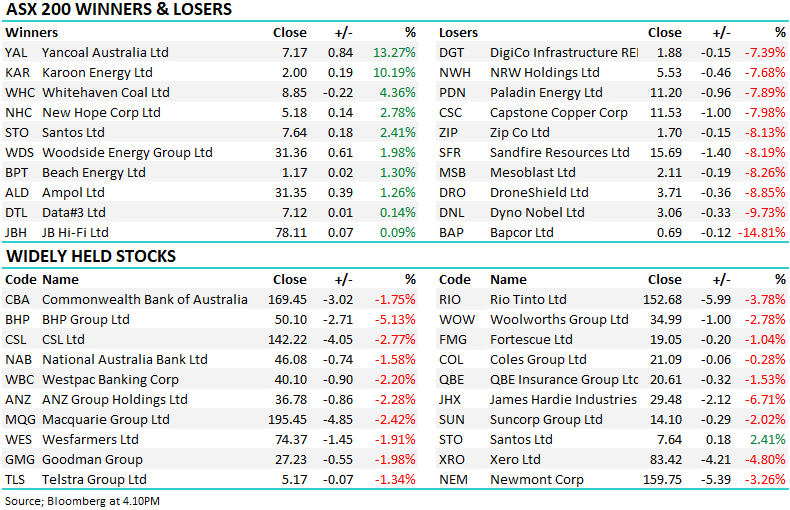

- The ASX 200 fell 252pts / -2.85% to close at 8,599

- Best performing sectors: Energy (+1.65%), Utilities (-1.18%), Communications (-1.89%)

- Worst performing sectors: Materials (-4.83%), IT (-4.76%), Industrials (-3.65%)

- Oil surged 26% to $US119/bbl — the highest levels since Russia’s invasion of Ukraine in 2022. Futures rallied a record 36% last week alone – more on this below.

- The three-year Australian bond yield hit 4.58%, a level not seen in over a decade. The 10-year punched through 5% for the first time since 2011. Markets are now pricing in a 37% chance of an RBA hike next week, with a move fully priced by May.

- The only real positive in an otherwise weak session was the ASX 200 bounced +140pts from the morning lows as buyers bought into the weakness.

- BHP (BHP) -5.13% was the biggest influence on the Index as economic growth fears hit the stock, but BHP is also contending with China’s CMRG effectively ordering traders to stop buying new BHP cargoes. Total losses over the past five sessions now exceed 16%.

- Rio Tinto (RIO) -3.78% and Fortescue (FMG) -1.04% also dragged lower, though FMG held up relatively better given Iron Ore prices were up ~2% on the day.

- ANZ (ANZ) -2.28% and the major banks — CBA -1.75%, NAB -1.58%, Westpac -2.20%, Macquarie -2.42% all fell. Rising bond yields and a deteriorating growth outlook are an uncomfortable combination for bank sentiment, even if the underlying businesses remain well capitalised. The sell-off feels indiscriminate at this stage but with yields moving the way they are, near-term pressure is hard to avoid.

- New Hope Coal (NHC) +2.78% — The standout in the Income Portfolio today. When gas supply is disrupted at this scale, coal benefits as an alternative baseload fuel and the market is pricing exactly that. Yancoal (YAL) surged 13.27% and Whitehaven (WHC) added 4.36% – which is held in the Growth Portfolio.

- Energy — Karoon Energy +10.19%, Santos +2.41%, Woodside +1.98%, Beach Energy +1.30% all higher, though gains were trimmed through the session as profit-taking kicked in. Santos and Beach Energy also confirmed they will proceed with the $357 million Moomba Central Optimisation project in the Cooper Basin – solid long-term news that was somewhat lost in the noise today.

- REITs and Rate-Sensitives is where the bond market move did the most damage. Goodman Group (GMG) -1.98%, Scentre (SCG) -3.58% and Mirvac (MGR) -2.89% as rising yields compressed valuations. Retailers felt it too — Wesfarmers (WES) -1.91% though JB Hi-Fi (JBH) inched up +0.09%.

- Gold was under pressure — Counterintuitively, gold fell as the USD rose and rising rate expectations overwhelmed the safe-haven bid. Northern Star (NST) -6.19% and Newmont (NEM) -3.26%.

- Dyno Nobel (DNL) -9.73% sold its Phosphate Hill fertiliser business to Mayfair Australia for $1, with up to $100 million in deferred performance payments, while funding ~$126 million in remediation costs before exit. The optics of a $1 sale price are always tough regardless of context. But Citi reiterated its Buy, pointing out Dyno is now a pure-play explosives business with FY26 EBIT guidance of $460–$500 million intact – the fertiliser drag is gone. Worth watching as the dust settles.

- DigiCo Infrastructure REIT (DGT) -7.39% had a double whammy today. CEO Michael Juniper stepped aside for extended personal leave with Chris Maher appointed interim CEO. Leadership uncertainty never helps, and the market sold first. DGT was also confirmed as being removed from the ASX 200 in the March quarterly rebalance effective the 23rd.

- Pro Medicus (PME) -0.90% was remarkably resilient all things considered. PME signed two five-year contract renewals in the US via Visage Imaging with a combined minimum value of $40 million. Solid execution continuing.

- Domino’s Pizza (DMP) -1.10% said Chairman Jack Cowin bought $3 million of stock on-market today, taking his stake past 25%. Incoming CEO Andrew Gregory (ex-McDonald’s) starts by August — there’s potentially a credible reset story building here.

- Bapcor (BAP) -14.81% was the worst performer in the ASX 200 today, a savage session with no specific news driving the move beyond broader rate-sensitive selling pressure amplified by thin liquidity.

- Qantas (QAN) -4.48% — Higher jet fuel costs continue to weigh.

- A difficult day across the board, though the Income Strategy held up best of the four strategies:

- Growth — down 2.7%, Income — down 1.2% the standout relative performer, Emerging Companies — down 3.2% & Core ETF — down 1.7%

- AUD/USD — $0.702 down (-0.20%) – was down 1% early

- Gold — ~$US5,132/oz, down $40 on the day

- Asian markets were weak; Nikkei in Japan -5.6%, Hong Kong -1.7% and China fell -0.9%

- US Futures are trading down ~1.7% – were down around 2% at the lows.

- Overall, todays move was aggressive, and we now believe it’s time to start adding some cash back into the market – with Oil potentially delivering a blow-off style top this morning, leading to a blow off style low in Equities.