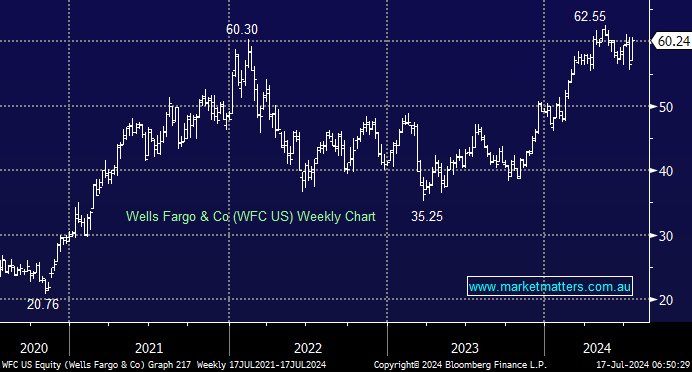

WFC reported quarterly earnings on Friday, and shares fell ~6% on the result, and while they’ve recovered, the trends were mixed for the 3rd largest bank in the US based on total assets. The bank’s Net Interest Income (NII), which measures the difference between interest revenues and interest expenses, came in at $11.92bn for the quarter, missing consensus by less than 2%. Revenue was a touch soft, and expenses a touch higher which weighed on margins.

Friday’s result shows WFC are still working through some regulatory issues (due to dodgy product sales a few years ago) that seem to be pressuring their ability to cut costs. Based on the company’s guidance, it looks like these pressures will remain for at least 2024.

- The share price recovery from Friday’s sell-off has been impressive and momentum, similar to many in the sector/market, which looks likely to take WFC to new 2024 highs, but it’s a move we’re more likely to fade than chase.

The bull thesis on banks centres around improving margins. Like any business that generates a lot of revenue, effectively managing costs can be very powerful. We’ve written before about the impact of technology/AI on improving a bank’s efficiency, and we think this remains an underestimated driver of future bank earnings, especially for banks that have consistently invested in technology over time – CBA the clear example in Australia.

US banks trade at a material discount to our own due in part to more competition, with WFC on 11x earnings and a price to book lower than all four Australian majors, and only slightly above BOQ and BEN. While WFC is no longer ‘cheap’, it’s around fair value relative to its peers, though earnings growth remains a challenge.

- We like the composition of WFC and UBS within the International Equities Portfolio for now; however, we now have a preference for UBS.

MM has turned more cautious on WFC above $US60

Add To Hit List