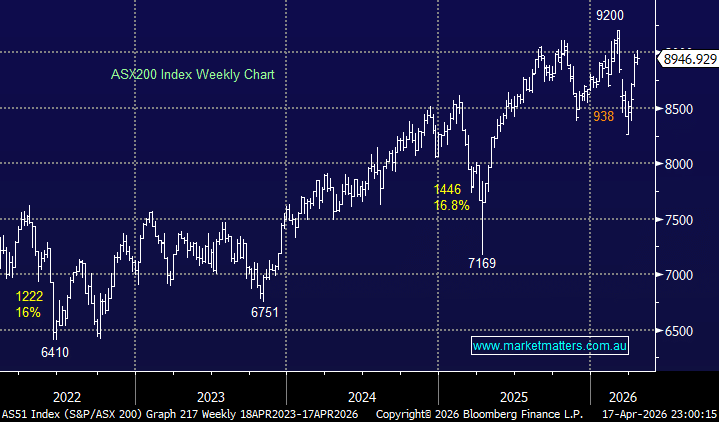

The ASX200 finished the week down -0.2%, snapping a 3-week winning streak as it failed to embrace the strength across global indices. A +13% surge by the tech sector wasn’t enough to offset losses by the influential banks, with the financial sector ending the week down -2.1%. Westpac set the tone early in the week, flagging that interest-rate volatility tied to the Iran conflict had hit its market’s income and prompted higher credit provisions. While not unexpected given rising rates, cost-of-living pressures and higher fuel prices, the update reinforced a cautious “if in doubt, get out” stance from investors ahead of May results from ANZ, NAB and Westpac.

The winner’s enclosure last week was dominated by the software stocks, which bounced sharply, in line with their US peers. Conversely, the losers’ enclosure was dotted with stocks that delivered negative corporate news to the market. Noticeably, the Iran War had little impact on the market:

Winners: Megaport Ltd (ASX:MP1) +26.5%, ZIP Co. (ASX:ZIP) +26.3%, WiseTech Global (ASX:WTC) +22.7%, Pro Medicus (ASX: PME) +17.2%, Pinnacle Investment (ASX:PIN) +16.8%, Paladin Energy (ASX:PDN) +15.5%, Xero (ASX:XRO) +14.7%, and SiteMinder (ASX:SDR) +13.3%.

Losers: a2 Milk (ASX:A2M) -19.2%, Downer EDI (ASX:DOW) -10.5%, Reece Ltd (ASX:REH) -10.4%, Temple & Webster (ASX:TPW) -9.5%, Westpac (ASX:WBC) -7.1%, Newmont Corp (ASX:NEM) -6.8%, Yancoal (ASX:YAL) -6.8%, and National Australia Bank (ASX:NAB) -6.2%.

Last week saw the market finally start to move on from Iran and focus on good old-fashioned earnings, company news and economics:

- The ASX started the week on the back foot after US–Iran peace talks collapsed over the weekend, with Trump announcing a naval blockade of the Strait of Hormuz—sending oil prices surging ~7%.

- Tuesday was the 1st of three consecutive sessions where the ASX200 opened above 9000, before surrendering much of the gains; this time it was all about Westpac’s cautionary update, which sent the bank down 2.6%, dragging ANZ and NAB in its wake.

- Wednesday was a similar story, although gold and tech stocks more than offset the drag caused by the banks and energy stocks as optimism around Iran gathered momentum.

- Thursday was a similar story on the index level, although it closed lower as a surging tech sector couldn’t offset broader losses across more influential stocks and sectors.

- On Friday night, global stocks surged after Iran declared open for business, sending the Dow up more than 860-points, setting Monday up for a 4th attempt to break clear of the 9000 level.

MM maintained a bullish bias through the volatile and unsettling March, expecting the ASX to be higher on June 30th and at Christmas. Importantly, now, even with US stocks surging to new highs and the ASX 200 index set to open around ~9000 on Monday, we remain bullish through 2026 and can easily see the local bourse testing 9500 later this year, and potentially higher. The basis of this being solid and resilient earnings growth.

Overseas markets closed the week with a bang after Iran announced the Strait of Hormuz was officially 100% open for business, with the tech-based NASDAQ enjoying its longest winning streak since 2013, and extending April’s advance to more than +12%. In Europe, the German DAX surged +2.3%, closely followed by the French CAC, which ended the session up +2%. In the US, the small-cap Russell 2000 index surged +2,1%, with the S&P 500 also enjoying a strong session, finishing up +1.2%.

- The SPI Futures are calling the ASX200 to open up +0.8%, back above 9000, following Friday’s strong session on Wall Street.