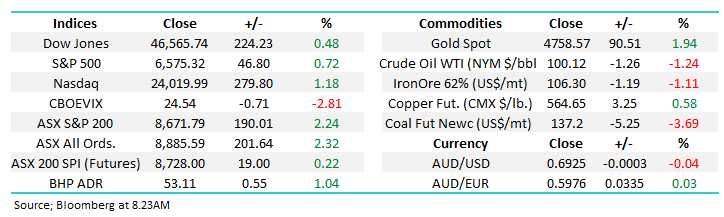

Having deliberately excluded miners, the turnaround potential across the four stocks reviewed today is likely to be modest, however:

- We like CBA for a solid +10% appreciation through 2026 plus an attractive dividend.

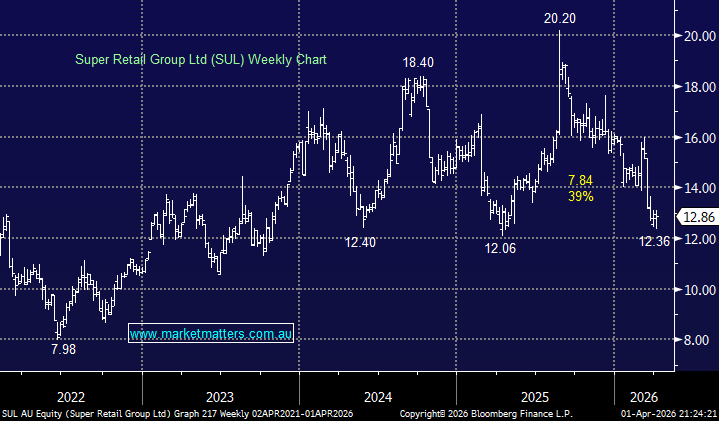

- We like SUL for a 20% recovery plus an attractive dividend in August assuming inflation fears improve sooner rather than later.

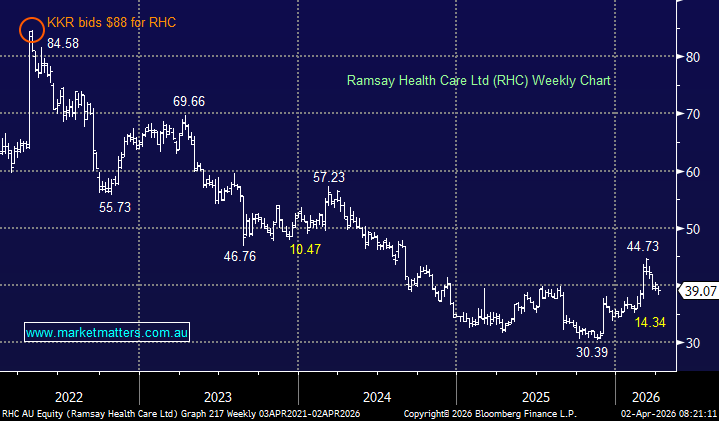

- We like RHC at these levels, though deescalation in the Middle-East and the post-war recovery that follows is likely to have less influence on the hospital operator.

- We like the risk/reward towards WOW back around $35 for this defensive turnaround story.