We see improving value in the rate-sensitive names but no reason to yet get overly aggressive:

- We like the risk/reward on offer in the real estate sector at present, but see no reason to go heavily overweight with the RBA still carrying a tightening bias – MGR is our top pick

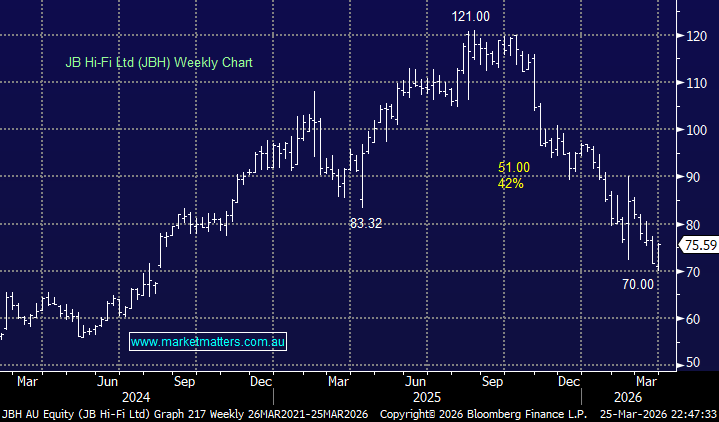

- Similarly in retail we like the risk/reward on offer, but see no reason to go heavily overweight just yet – we like both JBH and NCK.