Today we are facing a couple of new potential “bubbles” that could undo investors only considering the upside.

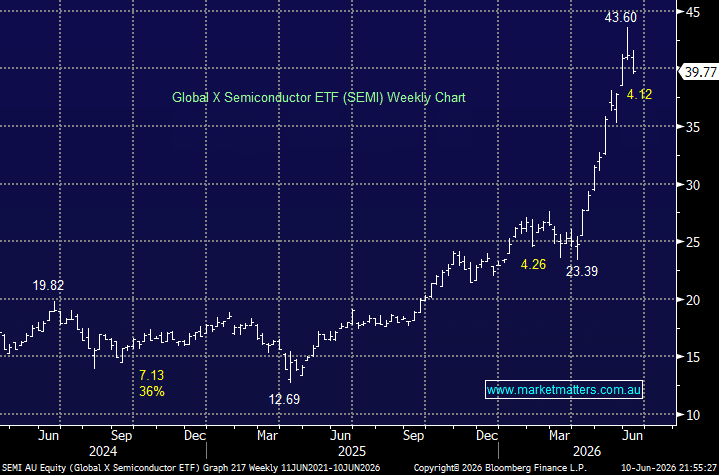

The “AI Trade” remains the market’s hot topic in terms of potential bubbles, with the ASX-listed SEMI ETF providing direct exposure to the infrastructure buildout through holdings such as Nvidia, Taiwan Semiconductor (TSMC), Broadcom, ASML, AMD and SK Hynix — the companies supplying the chips and equipment powering the global AI boom. As the digital equivalent of picks and shovels, these businesses continue to be among the largest beneficiaries of surging investment in data centres, cloud computing and artificial intelligence, helping the ETF soar almost 400% in the last year.

However, as we head into the “SpaceX” IPO and President Trump again banging his war drums, profit-taking is washing through the sector – the markets have gone from glass half-full to glass half-empty in a week, with the US iShares Semiconductor SOXX ETF closing more than 12% below last week’s high this morning. Another 5-10% on the downside, and we believe some excellent risk/reward buying will present itself for this growth sector.

- At MM, we believe in the “AI Trade”, but after surging higher over the last year, we prefer to buy dips as opposed to chasing strength.

While the AI Trade continues to dominate headlines, lithium has quietly become one of the market’s strongest-performing themes. The commodity and many of its related stocks have surged higher over the past year, in several cases delivering returns that exceed those generated by the AI winners, even after recent softness across the sector.

- Over the last 12-months: PLS Group (ASX: PLS) +324%, Liontown Resources (ASX: LTR) +188%, Mineral Resources (ASX: MIN) + 155%, and IGO Ltd (ASX: IGO) +97%.

The sector certainly hasn’t garnished the unbridled enthusiasm enjoyed by gold and Bitcoin before their demise, but as stock & sector reversion gather momentum, we felt this was an opportune time to revisit the sector, evaluating how we see it today from a risk/reward perspective.

- We believe the demand side of the equation is healthy for lithium as battery energy storage emerges as a 2nd pillar of lithium demand alongside EVs, driven by AI data centres and rising global investment in storage.

However, lithium supply is set to grow, with analysts split on when/if we experience a deficit, with some saying 2026/7 and others not until 2030. At MM, we remain bullish on the structural drivers that have lifted the spodumene price and expect these to continue throughout the cycle, with prices well above the 2026 highs a strong possibility, but after strong gains over the last 12 months, the risk is will incentivise new supply to hit the market sooner rather than later, coming from mouth balled operations that were put on ice as prices were weak in 2024-25 – implying that some consolidation at least looks likely.

- We wouldn’t be surprised to see Lithium rotate between $US2,000 and $US3,000 through 2026 after its ~300% appreciation.

This morning, we’ve looked at four stocks, with varying degrees of lithium exposure, all of which have enjoyed a cracking 12-months.