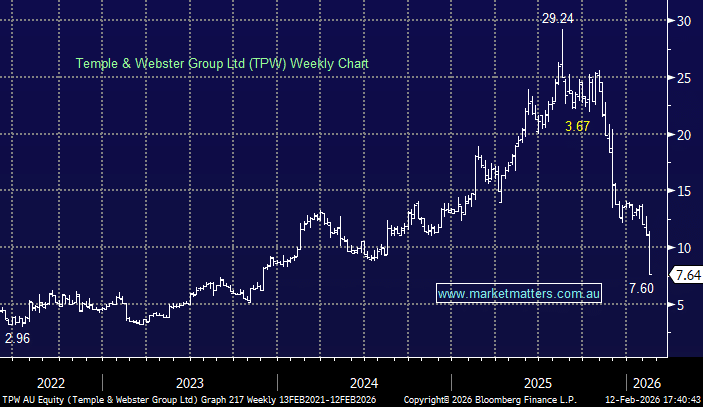

TPW –32.63%: Hit hard today after the online furniture retailer delivered a mixed 1H result. Revenue was broadly in line, showing solid growth, but the market zeroed in on weaker profitability, with gross margins falling short of expectations.

- Revenue of $375.9mn (+20% YoY)

- Net Income of $5.76mn (–36% YoY)

- Gross Margin at 31.4% vs 32.9% consensus

Management reiterated its longer-term ambition of reaching $1bn revenue by FY28, noting market share has climbed to a record 2.9% of the Australian furniture and homewares market. Early 2H trading looks solid, with revenue up 20% YoY from Jan 1 to Feb 9, supported by accelerating new customer growth, however the margin slippage is a clear sign that discounting is creeping back into the category.

There will likely be a bounce at some point but for now, this remains one to watch, until the company can rebuild confidence in their profitability.

MM is neutral toward TPW

Add To Hit List