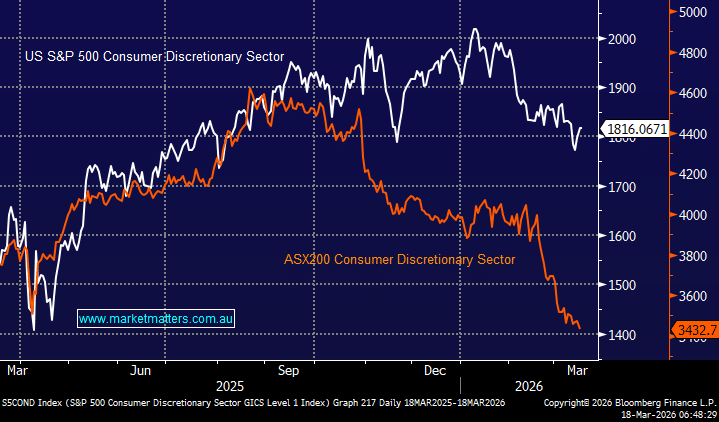

Rate-sensitive stocks have endured a shocking start to 2026, with the consumer discretionary sector (-13.8%) front and centre, especially considering the ASX200 has only slipped 1.2%, even with war raging in the Middle East. Amongst the sector itself, there have been no winners with a 7% retreat by Wesfarmers (WES) and 11% pullback by Premier Investments (PMV), the top performers, while Temple & Webster (TPW) -53% and Nick Scali (NCK) -33% are carrying the wooden spoon at this stage.

- The retailers have fared far better in the US as the Fed maintains an easing bias, as opposed to the RBA’s hiking cycle, i.e. interest rates impact spending.

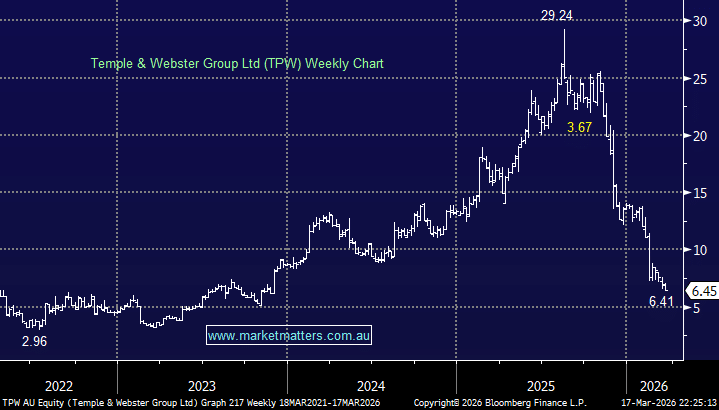

TPW may have become a household name over recent years, but it doesn’t mean its shares will appreciate. The online retailer has been at the forefront of the sector weakness, falling over 75% from its 2025 high as margins compressed, hurting earnings, even as revenue lifted. Last month, the stock was hit over 30% after its 1H result disappointed the market:

- Revenue rose 20% to $376m, but margins fell ~5% short of expectations, driving a steep earnings miss.

TPW has invested in pricing and promotions, helping sales but hurting margins. Total orders were up 14% and average order value increased 5%, however, discounting is driving much of this increase. Michele Bullock made this point yesterday – she spoke about Australians still spending, although they were clearly searching for bargains, a trend that’s likely to be amplified by yesterday’s rate hike.

Following last month’s result, management reiterated its FY28 target of $1bn in revenue, and early 2H trading has been strong, with revenue up 20% YoY, driven by accelerating new customer growth – that part of the equation looks fine. But if this is price sensitive growth, they’ll have a hard time lifting prices to improve margins, particularly in this environment.

- Last month was the stock’s second aggressive re-rate on the downside in less than six months, meeting a market that was bullish. TPW had 9 buys and 3 holds across the analyst community – ouch!

chart

US S&P 500 v ASX200 Consumer Discretionary Sectors

chart

US S&P 500 v ASX200 Consumer Discretionary Sectors

We see margins as the key to this stock. While they maintained margin guidance at the February update (FY26 EBITDA margin guidance reiterated at 3–5%), driving market share is their primary priority, even if it compresses margins near-term. This comes with obvious risks that need to be factored into our thinking.

TPW’s $775mn market cap is certainly more palatable than it was, underpinned by $376m in revenue, dropping down to a very small $5.8m profit. It’s trading well below its historical average valuation, yet it’s still expensive on traditional metrics, trading on a P/E of 67x for FY26, compared to 17x for JB Hi-Fi (JBH).

The Middle East conflict is now exposing TPW to rising freight costs, especially considering the large size and low density of its furniture, adding further weight to the company’s share price at a very inopportune time.

Overall, we like TPW’s growth profile, we’re just concerned about margin pressure and mounting headwinds to profitability. When we decide to increase our exposure to the retail sector for the Active Growth Portfolio, its likely to be simply increasing our JB Hi-Fi (JBH) holding.

- We can see TPW testing $6 in the coming weeks/months, but the risk/reward is emerging for aggressive investors.

MM is neutral towards TPW ~$6.50

Add To Hit List