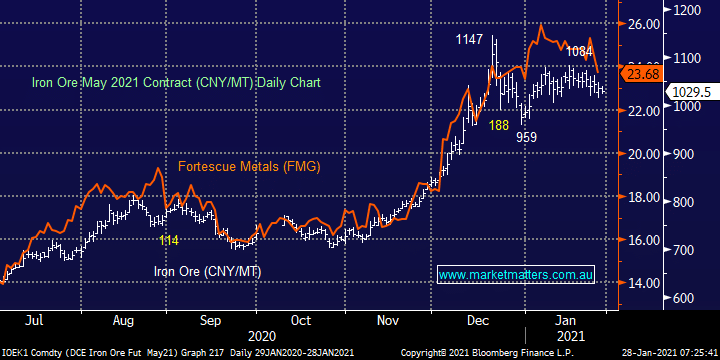

Iron ore has appreciated over 50% since late 2020 dragging the related sector significantly higher as non-believing analysts have needed to continually upgrade their revenue targets – a quick glance at the chart below should dispel any thoughts that stocks in the space don’t follow the price of the underlying bulk commodity. Obviously, China being the worlds largest steel producer is the key to the price of iron ore, it currently takes ~60% of its requirement from Australia but since the recent deterioration in trade between the two countries I’m sure they would like to reduce this dependency in the years ahead – China already has plans to start significant mining overseas by 2025.

At this stage of the cycle, MM still believes iron ore will go higher in 2021 as reflation takes hold with our initial downside targets a few % lower and 900 CNY/MT, the main question from our perspective is will the current consolidation provide opportunities in the sector.