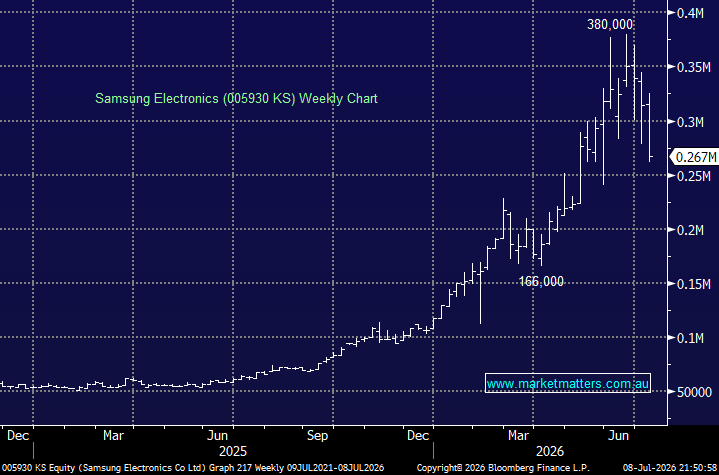

This week, Samsung has led the second wave of semiconductor weakness following its 1Q report, which beat expectations but wasn’t good enough to satisfy the crowded position that fled for the exits en masse – the stock has fallen 16.6% this week and 26.6% from its June high. Their result was certainly strong, but as we’ve discussed many times in the past, if everyone’s long, the risks around the share price are skewed to the downside.

- Record revenue: Samsung delivered record quarterly revenue of KRW133.9tn (~US$89bn), up 69% year-on-year—the highest in the company’s history and basically the equivalent to that of Apple Inc.

- Margins soared: Operating profit jumped 185% quarter-on-quarter to KRW57.2tn (US$38bn), with an exceptional 42.8% operating margin.

- AI drove the upside: The memory division posted a second consecutive record quarter, as booming demand for HBM and high-density DRAM reinforced Samsung’s central role in the global AI infrastructure buildout.

However, while the above reads exceptionally well, there’s been a massive headwind brewing: A wave of leveraged semiconductor ETFs have launched over the last 2 years, with more than US$80bn invested across these vehicles, which have endured an extremely uncomfortable few weeks, e.g. Direxion Daily Semiconductor Bull 3X (SOXS US), with over US$20bn in AUM, has tumbled 45% from its highs, again, demonstrating Greed is Not always Good!

However, the chart below shows Samsung remains well above its 2025 lows, having accelerated higher in the last 18 months, finally recognising the consistently rising revenue of one of the world’s largest chip manufacturers, and as the numbers above and chart below demonstrate, there is no smoke and mirrors here, but it’s an easy argument for the bears that the share price has risen too far, too fast, on leveraged momentum money:

- Over the last 5-years, Samsungs revenue has risen by just +12.5%, but its share price is up ~240%.

However, moving forward, expectations are high: The cumulative 3-year revenue growth implied by consensus is over +200%, demonstrating this is a quality growth company, creating the big question being what is a fair price to pay for its potential growth.

chart

Samsung Electronics Co., Ltd. (KRX: 005930) v Revenue – Source Bloomberg

chart

Samsung Electronics Co., Ltd. (KRX: 005930) v Revenue – Source Bloomberg

In the long run, share prices are driven by earnings but sentiment can have a huge impact, which in the case with Samsung prompting big swings in the stocks i.e. up and down 30% in a matter of weeks. At MM, we use a combination of macro influences, earnings and underlying financials to decide if we want to own a sector &/or stock, but in times of panic we use good old-fashioned experience & technicals to identify where we believe the panic liquidation (pain) will provide optimum entry opportunities.

The volatility might be scary, but with an estimated ~10% of Samsung and competitor SK Hynix held in leveraged ETFs, it’s hardly a surprise that such moves are occurring – short term it’s become like Bitcoin!

- In the case of Samsung, we like the risk/reward around 250,000, or 5-7% lower, i.e. where we feel leveraged unwind will again start to attract more sensible investors.

MM is bullish towards Samsung below KRW 250,000

Add To Hit List

chart

Samsung Electronics Co., Ltd. (KRX: 005930)

chart

Samsung Electronics Co., Ltd. (KRX: 005930)