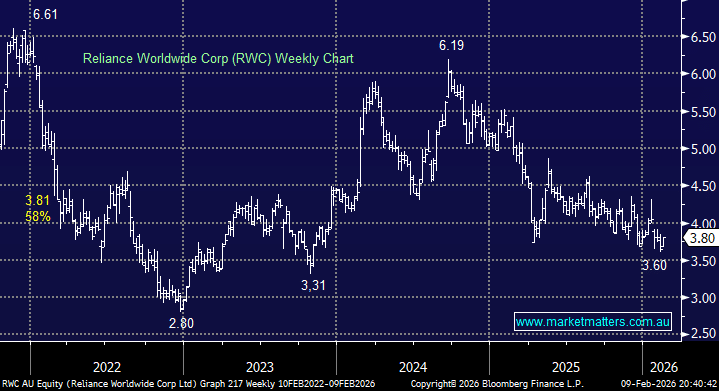

RWC has been under pressure as input costs surge – copper prices alone are up more than 30%, squeezing margins across the plumbing supply chain. The stock dipped last month following downgrades that centred on concerns around how aggressively RWC may need to lift prices simply to offset higher costs.

This remains a well-run business, but one facing cyclical headwinds largely outside its control. That said, rising copper prices are not unexpected, and while the pressure is real, we see this as more of a timing issue than a structural one, potentially creating opportunity for patient investors.

RWC is heavily US-exposed, with ~65% of FY25 earnings coming from the Americas and is currently dealing with the dual challenge of elevated input costs and softer housing conditions.

The company will face the market next week on 17th, and with the stock trading around 16% below its long-term valuation, expectations appear muted, leaving scope for upside if execution holds.

- We like the risk/reward at current levels, particularly for investors willing to look through near-term noise toward an eventual recovery in US housing.

MM is cautiously bullish towards RWC around $3.80

Add To Hit List