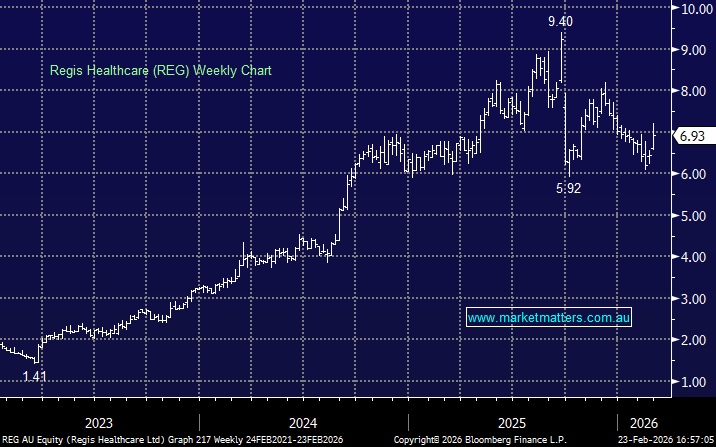

REG +7.6%: A strong first-half result drove solid gains despite acquisition costs weighing on statutory profit.

- Revenue $745m, +20% YoY, ahead of consensus

- EBITDA $125m, +8% YoY; underlying NPAT $29.7m, comfortably above expectations

- FY26 EBITDA guidance $130–135m reaffirmed

- FY28 target of 10,000 beds maintained, with growth via greenfields and acquisitions

A nice, solid update from the aged care provider today following a very choppy last 12 months where earnings have disappointed.

MM is cautiously bullish REG under $7.00

Add To Hit List