Plumbing business REH has struggled over the last few years as a mature ANZ market faces increasing competition and the US market remains challenging – at least for now. The US has been a tough backdrop for REH, where it generated over 55% of its revenue in FY25. The last quarterly update was better than feared bringing into question how much negativity is built into the company’s valuation – its trading more than 25% below its average 5-year valuation (EV/EBITDA). Additionally, the company has a $250m off-market buyback in play, with flexibility for up to $400m, which should help to at least support the stock.

- The company is due to report on the 23rd of this month, with investors looking for signs of improvement from its US business.

Overall, we believe REH provides attractive exposure to an eventual turnaround in the US construction market, with a management team arguably more aligned with investors than some others (i.e. James Hardie).

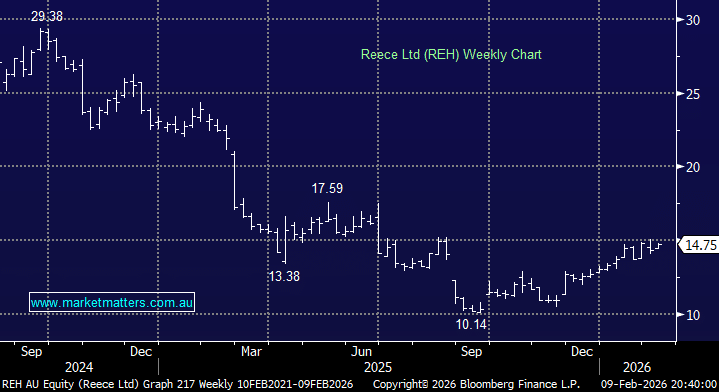

- We believe REH is offering deep value and solid risk/reward at current levels, although $15 does provide some short-term technical resistance.

MM is bullish towards REH around $14.75

Add To Hit List