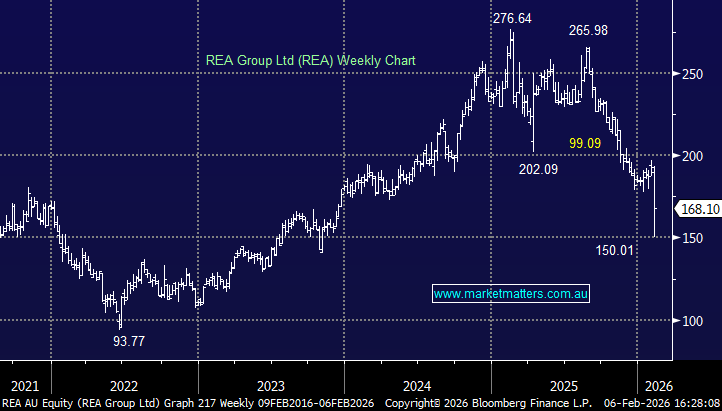

REA Group shares were sold heavily, down as much as 18% at their monring low, the sharpest fall since March 2020, after first-half earnings missed expectations and management flagged a decline in new listings into FY26. The result reinforces concern around listings momentum and near-term earnings risk, despite an otherwise resilient housing demand backdrop.

- Core net income: A$340.6m, +8.5% y/y (A$357m est.)

- Core revenue: A$915.8m, +4.9% y/y (A$935.6m est.)

- Core EBITDA: A$554.7m, +6.6% y/y (A$580.6m est.)

- Interim dividend: A$1.24 (A$1.10 pcp)

- EBITDA margin: 62% (61% pcp)

On a more positive front, they announced an on-market buyback up to $200m and said that buyer demand remains strong nationally; supply has improved in Sydney and Melbourne, supporting listings in those markets. FY26 national residential Buy listings now expected to decline 1–3%, reflecting larger-than-expected YTD weakness in Perth and Brisbane. January listings down 8% YoY (Sydney and Melbourne each -1%).

Positive operating jaws expected;

- Australia modestly positive. Opex growth unchanged at mid single digits (Australia high single digits)

- India EBITDA losses guided at A$40–45m; associate losses to improve modestly in FY26 vs FY25

The market reaction reflects a reset in expectations as listings momentum softens at the margin. While REA’s pricing power and margin structure remain solid, near-term earnings sensitivity to listings volumes has re-entered focus, particuarly at a time when compeition has emerged.

MM is neutral REA ~$160

Add To Hit List