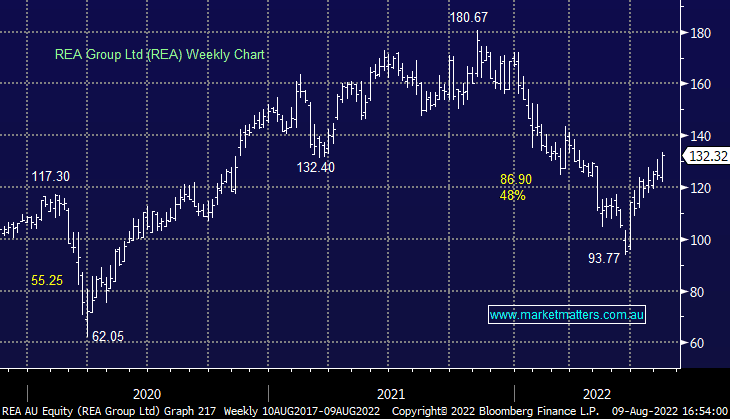

REA +6.69%: the property classifieds business announced their FY22 results today largely in line with expectations, with poor international performance offset by more bullish commentary. Revenue was $1.16b for the year, while Core EBITDA at $673.5m was a ~2% miss to consensus at $685m. Operating expenditure was up 11%, driven by wage inflation, new product development and marketing, though the market took a positive view that it will lead to more revenue. Guidance suggests these cost pressures should normalize in FY23. They have their work cut out for them, looking to integrate the recent acquisition of Mortgage Choice as well as putting the required investment into building their Indian business to be a market leader in that geography. Australian residential volumes have remained resilient into FY23 with volumes up 7% in July despite the broad negativity in the Aussie market. All in all a strong result and shareholders will receive an 89c div, up from 72c last year.

MM is now neutral REA around $130

Add To Hit List