QOR describes itself as a “cyber-safety and online-safety” / “digital-safety” company. It provides cyber-safety services to schools (student/child online safety, device filtering, parental controls) — so its core products are inherently cybersecurity-related. They make money by selling recurring subscription-based cyber-safety software, mainly to schools, with additional revenue from families/consumers, licensing partners, and rollout services. Broker commentary and external forecasts suggest FY27–FY28 as the more likely window for meaningful profitability — assuming continued subscription growth and cost discipline, but a lot can happen in that time.

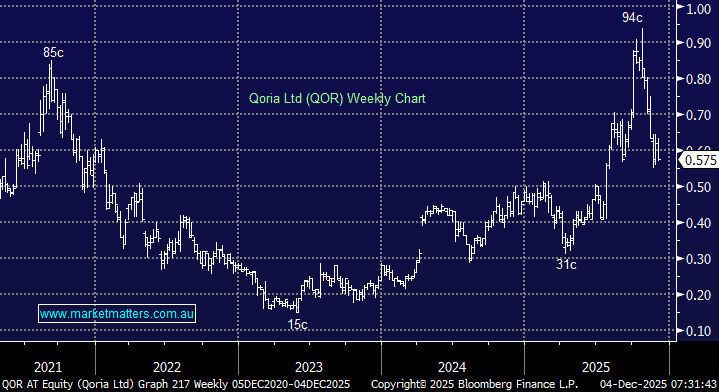

After reporting in October, the stock has plunged over 40% although it initially popped to new highs after lifting its FY26 revenue guidance – it’s tracked the likes of Xero and ASX big tech, which have endured major valuation contraction as rate cuts appear off the table. Competition is always fierce in growth areas, especially if revenue and margins are strong: several companies are lurking in the wings that could hinder QOR’s journey to profitability, including local competitors CyberCX, Tesserent/Thales, Senetas, FirstWave, and Prophecy, while the major global competitors are cybersecurity giants like Palo Alto Networks, CrowdStrike, Fortinet, Cisco, Microsoft, and Zscaler, which already dominate Australian enterprise and government cyber budgets.

- We are not keen on the risk/reward towards QOR in this rapidly evolving market.

MM is neutral towards QOR

Add To Hit List

Moving onto two global alternatives where things are arguably bigger and better, something that is not always the case!