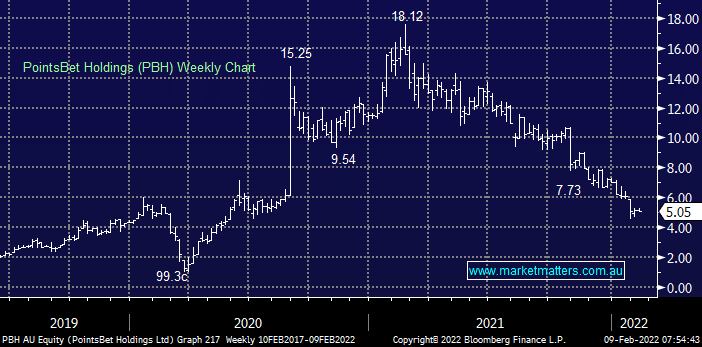

The online wagering business has a solid operation in Australia however they are aggressively targeting the growing US betting market thanks to changing US state laws that are allowing mobile sports betting & iGaming.

Since peaking a year ago above $17, PBH raised $215m in an institutional placement at $10.00 followed by an entitlement offer at $8.00 to existing shareholders that raised a further ~$185m – shares have been under pressure ever since. It is clear that PBH see a big opportunity and they are going hard at it, however it’s also clear that the cost to acquire customers is increasing given stiff competition which has seen the level of cash burn increase in the last quarter. They have $569m in cash at the end of the quarter, a good war chest in the battle for punters bets which accounts for a large portion of their ~$1.3b market capitalisation. They also own their own technology platform which is extremely valuable when looking to scale in this sector, plus they have acquired valuable licenses to operate.

We simply believe that PBH is too cheap for the strategic value in the business making it a strong takeover candidate in a space that’s seen plenty of consolidation.

MM remains optimistic PBH despite share price weakness

Add To Hit List