MP Materials Corp. is about 10% larger than Lynas, having underperformed its ASX peer so far this year. The Las Vegas-based business operates the Mountain Pass mine in California, currently the only integrated rare-earth mining and processing facility in the U.S., with the company’s core output being Neodymium-Praseodymium (NdPr). With the U.S. Department of Defence now its largest shareholder and a recent $US500 million magnet supply agreement with Apple, MP Materials is positioned as a strategic cornerstone in efforts to secure and diversify America’s rare-earth supply chain.

Like many in the space, MP Materials Corp. is not profitable. In 2Q25, the company reported a net loss of $US30.9 million, but forecasts suggest MP Materials is expected to deliver earnings growth of ~50‑60% annually over the next few years (obviously from a low base), as revenue continues to grow, with 2Q25 producing $US57.4 million, driven by record production and the commencement of magnetics production.

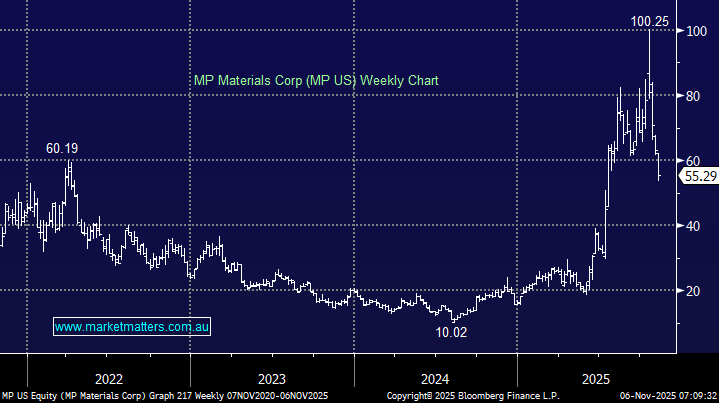

- We like the risk/reward towards MP back below $US60, but like its peers, it’s likely to be a volatile ride.