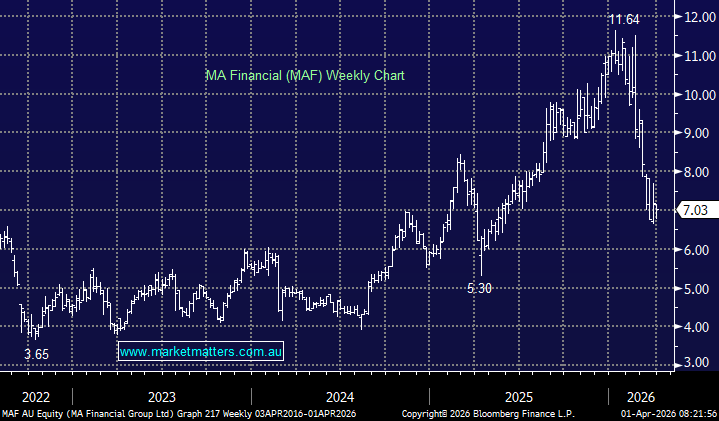

We’ve been doing more work on MA Financial (MAF) and, while we’re not ready to pull the trigger just yet, we’re adding it to the Hitlist for the Emerging Companies Portfolio. For readers less familiar with the name, MA Financial is a diversified financials group with exposure across asset management, private credit, lending, corporate advisory and broader financial services. It also has meaningful exposure to real assets, owning and managing hotels and accommodation, marinas, shopping centres, industrial and logistics assets, as well as health and aged care facilities, making it a broad play on several parts of the Australian economy. Unsurprisingly, in periods of market stress, asset managers tend to be sold down, and that’s certainly been the case here, with MAF off around 40% from its recent highs – and that’s what has us interested.

It’s not a new story, though it is becoming a better one. Private credit has clearly been in the spotlight recently, but it’s important to distinguish MA from some of the issues emerging offshore. Much of the recent concern has centred on US private credit, particularly exposure to software and more aggressive corporate lending, whereas MA is more focused on real assets and asset-backed lending, which we see as a different and, in many cases, more tangible part of the market.

Over the past decade, MAF has steadily shifted away from the more cyclical, transaction-heavy earnings streams that come with traditional corporate advisory, and towards businesses with stronger recurring revenue and better visibility, namely asset management, lending and broader financial services. Advisory can be highly profitable when markets are buoyant and deals are flowing, but it is also notoriously fickle. What MA is building today looks far more resilient than the business many investors probably still associate it with. Increasingly, this looks like a more diversified, scalable and higher-quality financial platform, with a larger share of earnings coming from areas that should prove more durable through the cycle.

What appeals to us most is the company’s focus on capability over theme. In other words, this is not simply a business gathering assets and clipping fees. In areas like private credit, real estate and lending, MA is sourcing, underwriting, structuring and, in many cases, managing the underlying assets in a hands-on way. That matters because these are not commoditised businesses when executed well. The value sits in the skill set, the network and the ability to originate attractive opportunities, not simply in having exposure to a fashionable part of the market.

Importantly, the numbers are now starting to reflect that evolution. The better-quality parts of the business are becoming more prominent, which gives us greater comfort that this is more than just a good story. In our view, the market still may not fully appreciate how far MA has moved away from its old advisory-led roots.

Of course, it’s not without risk. This remains a financial business, meaning it won’t be immune to weaker credit conditions, softer asset values, tighter funding markets or a slowdown in transaction activity.

Understanding gearing is also important in a business like this because too much leverage is often what causes problems. MA does use leverage, though much of the apparent debt reflects funding inside non-recourse lending vehicles rather than aggressive balance-sheet risk at the listed parent level. Stripping out the debt housed inside non-recourse lending trusts and warehouse structures used to fund mortgages, receivables and other credit assets, MAF has cash of around $30m, corporate debt of ~$159m, and an undrawn revolving debt facility of $55m.

In balance sheet terms, MAF sits somewhere in the middle. It is more geared than a pure asset manager, less stretched than a typical non-bank lender, and a long way below the structural leverage of a traditional bank, given much of the debt is housed in non-recourse funding vehicles rather than the listed parent itself. On that basis, we are comfortable with the current level of gearing.

From a valuation perspective, MAF now trades on around 14x, roughly 1 standard deviation cheap relative to its five-year history. The recent sell-off has driven a meaningful de-rating, with the stock moving from around 21x down to 14x, despite the business continuing to grow. FUM is rising, earnings momentum remains strong, and that is helping underpin a solid growth outlook. FY25 earnings grew by 35%, with consensus expecting +55% in FY26, before moderating to the high teens from FY27 onwards. On those numbers, the stock screens as inexpensive over the medium term, falling to around 10x by FY28, while offering a fully franked yield that we think will move from roughly 3% today to around 5% over time.

- We are bullish on MAF from current levels. The only real reservation is portfolio construction, given we already own Pinnacle (PNI) and Regal Partners (RPL), which would create a meaningful degree of correlation. Still, on its own merits, this is a stock we think is attractive.

MM is bullish MAF ~$7

Add To Hit List