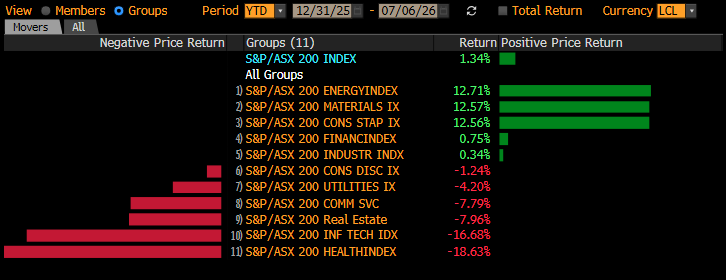

Moving onto the ASX where the investment landscape may be a touch trickier when we cast the net further afield than the resources, although if they follow in the footsteps of the US, there is some meaningful performance catch-up to be made on the stock and sector level. When we look at the Advance-Decline Ratio (A-D) below, things are permeating through.

NB The advance-decline ratio measures market breadth by comparing the number of stocks rising with the number falling on a given day.

The A-D line (bottom panel in blue) has broadly confirmed the index’s direction, with the most important signal being the A-D line making new highs in Jan–Feb 2026 alongside the index pushing through 9,000–9,200, textbook confirmation of broad participation. The March 2026 selloff saw both the index and A-D line deteriorate in tandem, and the subsequent recovery has the A-D line back near cycle highs as of early July 2026, even as the index sits ~4% below its Feb peak, a positive breadth divergence that supports the broadening thesis.

We like the “generals and soldiers” analogy when looking at broadening gains in stock markets: for much of the past year, the generals (AI mega-caps) carried the market, but now the soldiers are finally joining the advance. Bull markets rarely end because leadership broadens; they usually end when participation narrows. In that sense, the best news for the AI trade is that the market no longer needs it to rally, reducing concentration risk and creating a healthier foundation for further gains.

It is important before we bore into the ASX200 to add a caveat that could trigger us to be wrong: another rate hike leg, an energy re-spike from the Middle East, or breadth rolling over within weeks (early-cycle broadening attempts often fail once or twice before one sticks). The latter is similar to how MM often describes a market “looking for a low.”

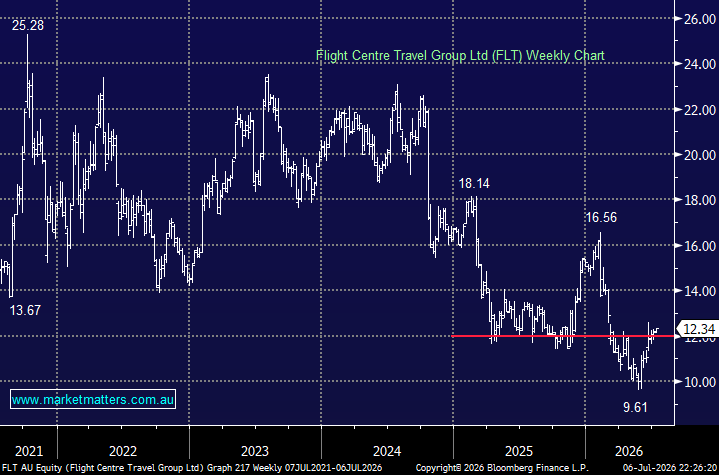

- This morning we’ve looked for three opportunities from the underperforming sectors below that are already enjoying a change in fortune as investors look for value in what’s been a very polarised market.

The RBA cash rate remains the single biggest determinant of how broad any ASX rally can become. A dovish pivot would likely ignite REITs, Consumer Staples and Discretionary, but without a pivot, the rally is more likely to remain concentrated in Resources, Industrials & Financials.

The highest-conviction, rate-agnostic catch-up plays on the ASX are therefore Materials/Resources (structural copper deficit) and Financials (40% of index earnings, 5–7% revenue growth to 2029, not in downgrade mode). Both work regardless of what the RBA does next. However, until we get a sniff that the housing market has bottomed, the financials, and in particular the banks, will struggle to garner investor attention, especially as they’re not cheap from a historical perspective.

A throwaway thought is the “Big Four Banks” pay an attractive yield with definite exposure to Australian property, since the Budget we believe they’re arguably a better investment than investment property until further notice. However, this morning we’ve “Kept It Simple Stupid” looking at three stocks that have already turned, have varying degrees of US exposure, and still screen well if the market broadening does continue.