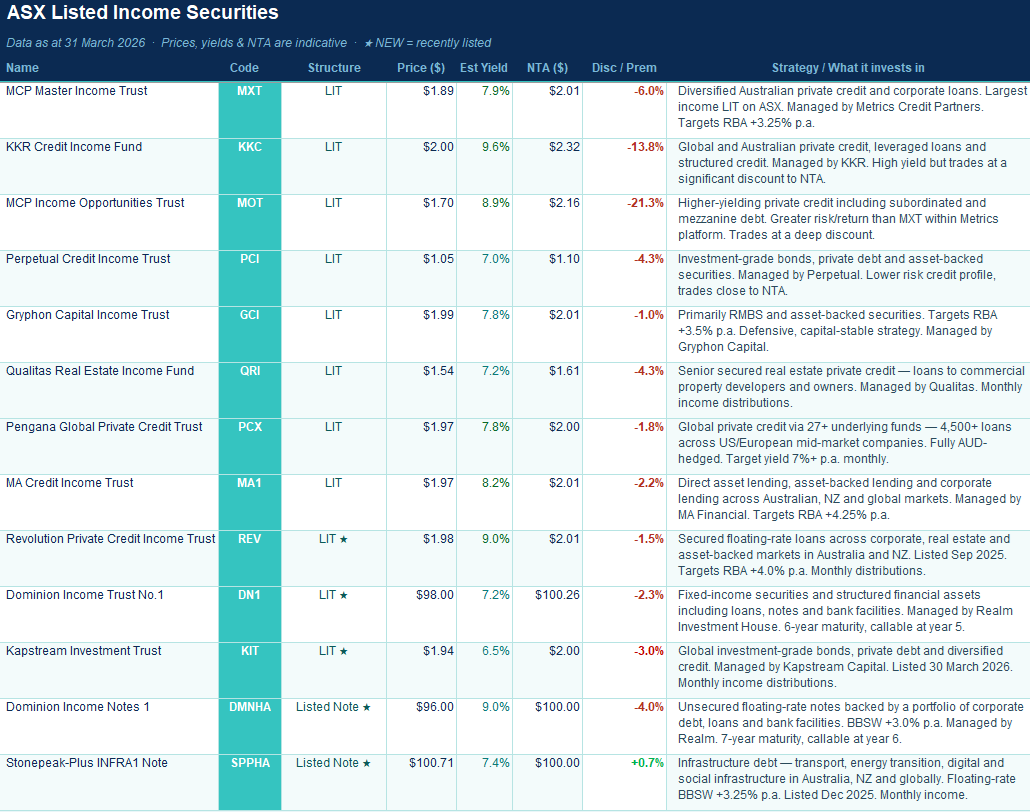

The ASX-listed income space continues to offer investors an appealing alternative to traditional fixed income, term deposits and even parts of the equity market, particularly for those seeking regular cash flow in a still-uncertain macro backdrop. Yields across the sector are generally sitting in the 7% to 10% range as shown in the table below, with most vehicles also trading at a discount to their underlying asset value (NTA), which on the surface at least, makes the area look attractive.

That said, as is so often the case in markets, the headline yield rarely tells the full story. When looking at listed income securities, we think there are really two buckets investors need to separate from the outset: those with a defined maturity date, and those that are effectively open-ended / perpetual listed trusts. It’s an important distinction, because while both might sit in the same broad income universe, the way they behave, and the risks investors are taking, can be very different.

The first split: maturity date versus perpetual capital

The listed notes and dated vehicles are generally easier to underwrite. If the manager does their job, the assets perform and markets remain functional, investors have a clearer pathway to getting capital back at or around face value over time. In the list below, this includes names such as Dominion Income Trust No.1 (ASX:DN1), Dominion Income Notes 1 (ASX:DMNHA) and Stonepeak-Plus INFRA1 Note (ASX:SPPHA), all of which have finite terms. That maturity profile can help anchor value and often limits how far discounts can persist, provided credit quality remains sound.

That is a different proposition to the more traditional LIT structure, where there is no natural maturity event to pull the price back toward NTA. In those vehicles, investors are far more reliant on secondary market demand, portfolio performance and manager reputation to close discounts over time. Good assets can still trade cheaply for extended periods, and we’ve seen that play out across a number of credit and private debt names.

- That doesn’t make perpetual LITs bad investments, far from it, but it does mean investors need to be comfortable owning a vehicle where the discount may remain part of the investment experience, even when the underlying portfolio performs as expected.

Discounts are attractive, but often reflect risk

One of the most striking features of the current landscape is the size of some discounts on offer. KKR Credit Income Fund (ASX:KKC) at around a 14% discount, and MCP Income Opportunities Trust (ASX:MOT) which is trading over 20% below NTA, immediately stand out. Those are big numbers and they will naturally attract attention from yield-focused investors. But there’s usually a reason.

Higher stated yields and deeper discounts often come with higher-octane exposures underneath – more subordinated credit, more mezzanine-style risk, more complexity, or simply a more aggressive part of the private credit spectrum. MOT, for instance, offers one of the more compelling headline yields in the sector, though that comes with greater risk than the more vanilla exposures inside MXT. Similarly, KKC’s higher yield and larger discount reflect the market’s view of the underlying strategy, which spans global and Australian private credit, leveraged loans and structured credit. There may well be value there, but it is not “free yield”.

- We like the sector, though we’ve generally avoided the higher-octane end of listed income, preferring exposures where the income stream is supported by better asset quality, stronger diversification and a simpler path to capital preservation.

For inves3tors looking for a more conservative entry point into the sector, the more defensive names remain the easiest to get comfortable with. Metrics Master Income Trust (MXT) is the largest in the space at about $2.4bn and has been the go too for many investors. We turned more cautious on this security a few years ago for two main reasons. 1. we saw the credit quality of their underlying loans decline & 2. We think their size is a headwind, almost forcing them to participate in deals to allocate their vast amounts of capital.

Perpetual Credit Income Trust (ASX:PCI), which we hold in the Income Portfolio, and Gryphon Capital Income Trust (ASX:GCI) also sit toward the lower-risk end of the listed income universe, in our view. PCI’s exposure to investment-grade bonds, private debt and asset-backed securities makes it one of the steadier options, while Gryphon’s focus on prime RMBS and asset-backed securities gives investors a more defensive, capital-stable profile. The yields are not the highest in the sector, though that trade-off looks sensible given the quality of the underlying assets.

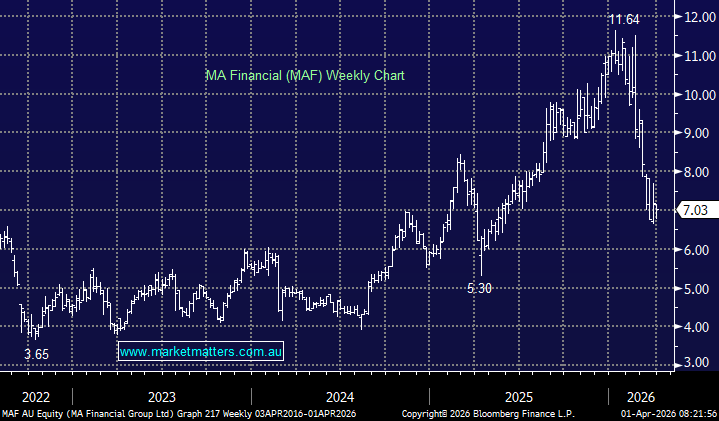

MA1 is one of the newer entrants to the listed private credit space, having listed in March 2025. Managed by MA Financial Group (ASX:MAF) – a well-regarded Australian alternative asset manager (also covered in today’s note), targets RBA Cash Rate +4.25% p.a. and has been delivering on that promise since inception. The strategy is genuinely diversified across direct asset lending, asset-backed lending and direct corporate lending, with exposure to Australian, New Zealand and selective global opportunities. What distinguishes MA1 from peers is the degree of manager alignment. MA Financial has significant skin in the game, and the proprietary deal origination through relationships built over many years in the mid-market lending space. They also have a quarterly off-market buy-back feature (borrowed from PCX’s playbook) whereby investors can tender in units at NTA, which also helps underpin the unit price, though this mechanism is capped at 5% of issued capital per quarter.

At the other end, the names with the highest headline returns often require a lot more selectivity. MOT, KKC, and arguably some of the newer or more bespoke offerings can work well in the right environment, though we think they need to be treated as part of the opportunistic sleeve rather than the core of an income allocation.

Maturity can improve the proposition

One area that is becoming more interesting is the emergence of dated listed income securities, because they offer a hybrid appeal: strong running yield, listed liquidity, and a clearer maturity profile than the traditional LIT structure.

That can be particularly useful in a market where investors are still wary of getting trapped in a perpetual discount. With a maturity date attached, we are not relying solely on market sentiment to unlock value. Over time, assuming the credit performs, there is an embedded mechanism for capital to be returned.

That said, maturity alone is not enough. Investors still need to look through to the underlying assets, ranking in the structure, term, manager quality and whether the yield is compensating appropriately for the risks involved. A seven-year note backed by weaker credit is not automatically safer than a high-quality LIT simply because it matures.

Prices and yields as of 31 March 2026. Yields may be vary, and are stated targets or prevailing running yields only. NTA is at the last reported date for each security – some are daily, some monthly. Newer securities as denoted with a star, have been listed less than 6 months.

Overall, we continue to like the ASX-listed income sector, particularly as a source of diversification and regular cash flow, but we think the area needs to be approached with more nuance than simply chasing the highest number in the yield column.

For us, the most important filters are: structure, asset quality, manager quality and where the strategy sits on the risk spectrum.

The split between maturity-dated securities and perpetual LITs is a useful starting point. Dated structures can provide an added level of comfort around capital outcomes, while perpetual trusts can still offer attractive value, albeit with greater reliance on market sentiment and discount management over time.

- Our preference remains to stay closer to the core, better diversified and less aggressive end of the sector, even if that means giving up a little headline yield. In income investing, preserving capital and sleeping well at night still matters more than squeezing out the last 100bps.

- We currently own: PCI, DN1, and are positive on MA1, SPPHA (on weakness below par) & DMNHA.

Of the securities trading at the deepest discounts, we prefer MOT over KKC given domestic rather than international exposures, though both are interesting for higher risk investors given the steep prevailing discount to NTA. There will be growing pressure on the managers to reduce that discount over time, and we may even see a de-listing event, where the portfolio is realised near NTA and investors receive back cash, similar to what Neuberger Berman did a few years ago with the NB Global Corporate Income Trust (ASX: NBI) – although we would certainly not make this the basis for investing in either, particularly when MOT is around 2x the size of NBI.