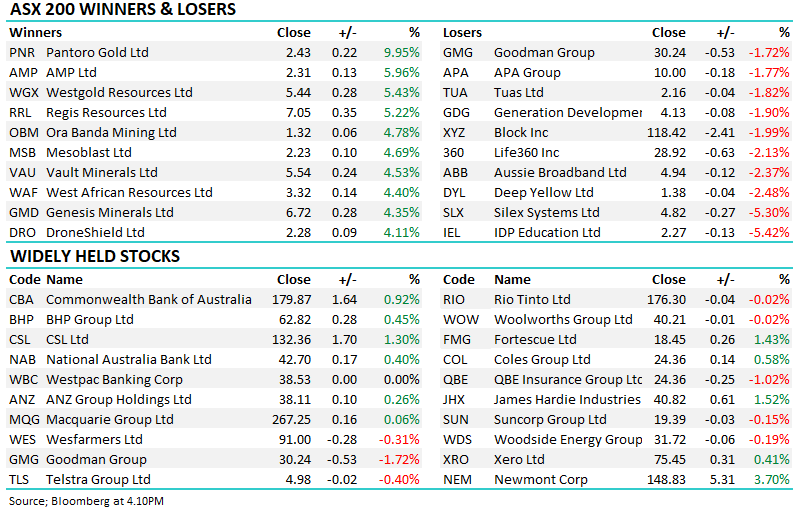

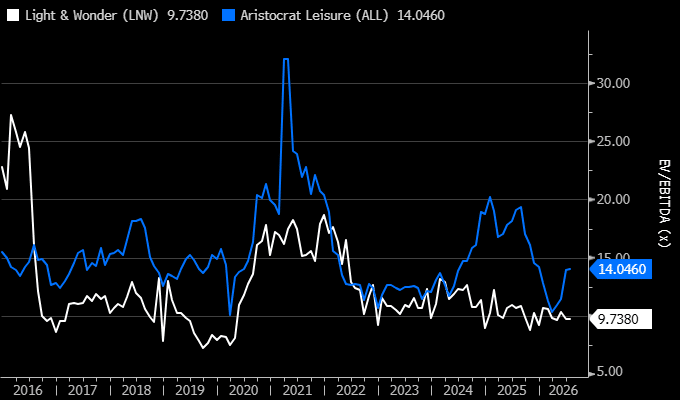

Yesterday saw Light & Wonder surge as much as 10%, its biggest intraday gain since early May, after reassuring investors on both earnings and growth – these gains were maintained in US trade overnight. The catalyst for the gains was management reaffirming FY26 guidance for mid-to-high single-digit earnings (AEBITDA) growth, while reiterating plans to reduce leverage below 3x net debt/EBITDA in the first half of FY27 and confirming US$180m remains under its share buyback program.

- LNW is trading well below its long-term valuation, which is more aligned with a downgrade, which we believe isn’t justified following yesterday’s announcement,

Rival Aristocrat (ALL) is trading up more than 35% from its 2026 low following an earnings beat (~2.3%) in May and guidance being reaffirmed in late June; we can now see LNW following a similar path in the coming months. LNW has been a frustrating ride for MM, but we did like yesterday’s update and will give our position some room at current levels.

- We like the risk/reward towards LNW around $112, expecting it to re-rate similarly to ALL.

MM is now bullish towards LNW around $112

Add To Hit List

chart

Valuations of Light & Wonder Inc (LNW) v Aristocrat Leisure (ALL) – Source Bloomberg

chart

Valuations of Light & Wonder Inc (LNW) v Aristocrat Leisure (ALL) – Source Bloomberg