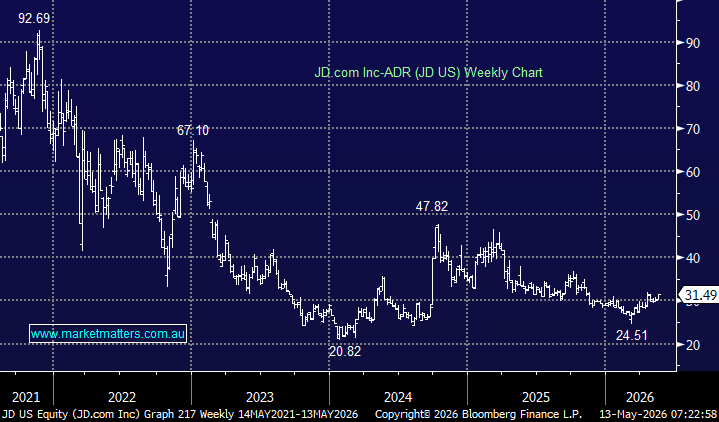

JD.com delivered a better-than-expected March quarter result overnight, with revenue and profit ahead of expectations, while the key positive was evidence that losses in its newer businesses, particularly food delivery, are narrowing. We own JD.com in the International Equities Portfolio, and while the stock has been weighed down by concerns around China’s consumer backdrop and aggressive food-delivery competition, this result should help rebuild some confidence that the core retail business remains profitable and management is getting better control of investment spend.

March quarter highlights:

- Revenue rose 4.9% YoY to RMB315.7bn, ahead of expectations for RMB310.1bn.

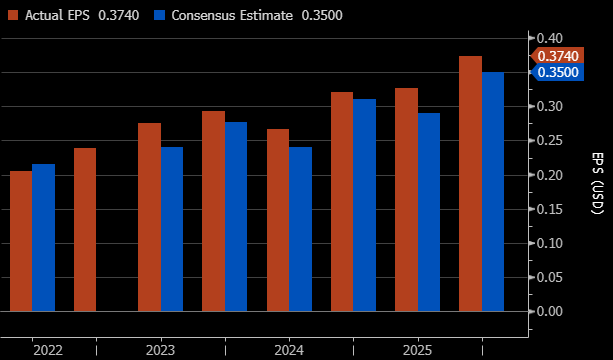

- Adjusted net income was RMB7.4bn, down 42% YoY, but well ahead of expectations for RMB5.3bn.

- Net profit was RMB5.1bn, reversing the RMB2.7bn loss recorded in the December quarter.

- JD Retail revenue rose 1.8%, a modest outcome, but the division remained very profitable.

- JD Retail operating profit increased 17% YoY to RMB15bn, with margin improving to 5.6% from 4.9%.

- JD Logistics revenue rose 29%, with margins also holding up better than feared.

- New business revenue increased 9.1%, with losses narrowing sequentially, led by food delivery.

- Food delivery unit economics improved, and investment losses narrowed materially versus the prior quarter.

The key issue for JD has been whether its push into food delivery would permanently dilute group profitability. Competition in China’s delivery market remains intense, with JD taking on Meituan and Alibaba’s Ele.me through heavy discounting, but the March quarter suggests the worst of the earnings pressure is probably behind it. Management said food delivery continued to develop healthily, unit economics improved, and investment in the segment narrowed significantly on a sequential basis.

Importantly, JD’s core retail business is still doing really well. Retail sales growth was subdued at +1.8%, but operating profit growth of 17% and margin expansion to 5.6% was a good outcome given the competitive backdrop. The mix shift helped, with a greater contribution from higher-margin general merchandise, marketplace and advertising services, while electronics and home appliances became a smaller part of the revenue base.

This is important because our investment case for JD is not about rapid top-line growth. It is about whether the company can compound earnings from a stronger retail platform, monetise its logistics advantage, and selectively invest in adjacent categories without destroying shareholder value in the process. On that front, this was a cleaner result.

The other positive was logistics. JD Logistics grew revenue strongly and held margins despite absorbing some external food-delivery operations. That reinforces the strategic value of JD’s supply chain infrastructure, which remains a key differentiator versus more asset-light e-commerce peers.

While headline growth is still modest, adjusted profit was lower year-on-year, and competition in Chinese e-commerce and food delivery remains fierce, this was a better the result in the things that matter: core retail margins improved, food-delivery losses narrowed, logistics performed well, and the group returned to profit after the December quarter loss.

- JD is trading on just 9.2x earnings – a steep discount to it’s own history, against earnings growth expected to be ~14% in FY26 (Dec year-end), jumping to the 20% range in outer years as food delivery increases profitability. We think JD is a compelling buy.

MM remains long & bullish JD ~$US31

Add To Hit List