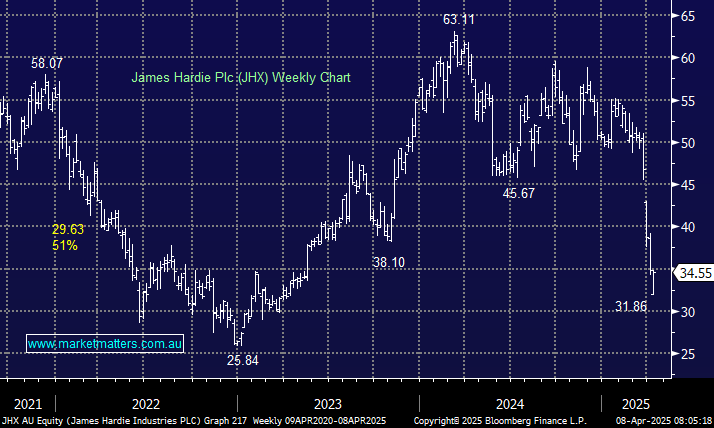

JHX has been hit hard in recent weeks following the company’s acquisition of AZEK Company Inc., a U.S.-based manufacturer of outdoor building products, a deal valued at approximately $US8.75 billion. We and the market are sceptical of the acquisition, and especially the price paid, which cynically appears favourable to the board and unfavourable to shareholders – we’ve heard that before! There are still risks to the deal from the likes of regulatory approval and aggressive investor backlash, but it is probably wishful thinking that Aaron Erter and Anne Lloyd will pay any attention to the people they effectively work for.

However, moving on, JHX generates 74% of its revenue in the US and is now trading close to 40% below its average valuation over the last 5-years. We believe the stock is great value at current levels even after the disappointing purchase of AZEK, assuming the board plans to the “right thing” moving forward.

- We like JHX from a risk/reward perspective below $35: MM owns JHX in our Active Growth Portfolio.

MM remains long and cautiously bullish JHX

Add To Hit List