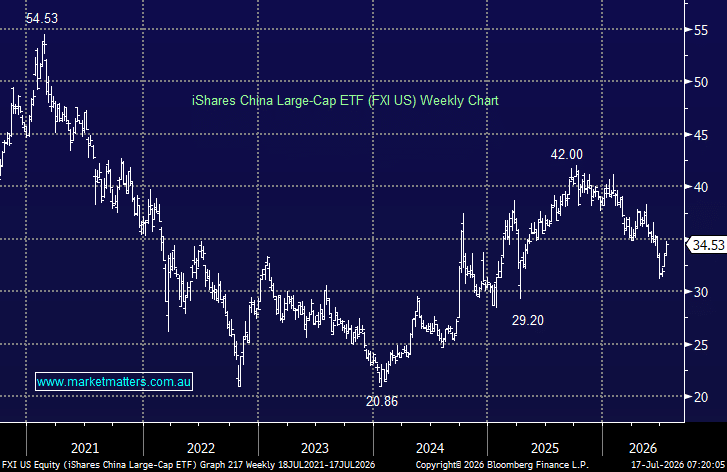

As the name implies, the iShares China Large-Cap ETF (NYSE: FXI) provides exposure to China’s largest listed companies, primarily financials, internet, energy and consumer businesses, offering investors a liquid way to access the country’s blue-chip equity market.

The FXCI ETF has now experienced its fifth straight day of outflows totalling $350.9m, taking its AUM to the lowest in at least a year. It’s been an interesting story, albeit a differing one of money flow across Asian ETFs:

South Korea (EWY) is the standout geographic story — five consecutive days of inflows suggest a strong rotation into Korean equities is ongoing, likely driven by semiconductor exposure (Samsung, SK Hynix).

China (FXI) is seeing the opposite — five straight days of outflows despite China’s National Team ETFs recording their largest inflows in 15 months on Monday as domestic authorities stepped in to support markets.

The flow divergence between these two Emerging Markets ETFs tells an interesting story of shifting investor sentiment across Asia

iShares China Large-Cap ETF (FXI US)

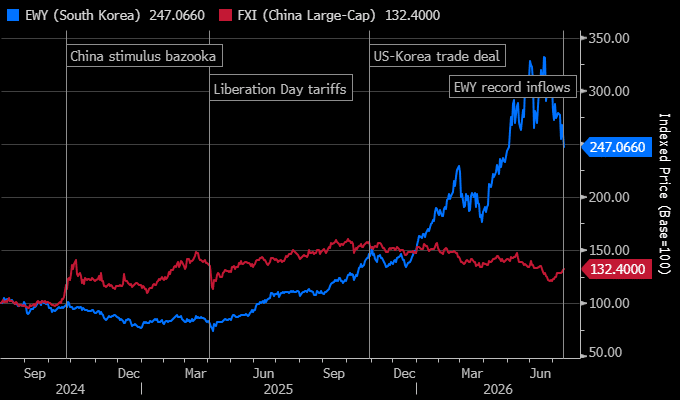

- China stimulus spike (Oct 2024): The FXI recorded a massive ~$5.1bn inflow in October 2024 following Beijing’s sweeping stimulus package announcement. This was rapidly reversed, with ~$2.3bn flowing back out in November 2024 as enthusiasm faded.

- Persistent outflows since: From late 2024 through mid-2026, FXI has seen almost uninterrupted outflows. June and July 2026 alone have seen ~$1.1bn exit, with AUM at its lowest level in at least a year.

- Tariff shock (Apr 2025): FXI suffered its second-largest monthly outflow of the period (~$1.3bn) as US-China trade tensions escalated sharply.

iShares South Korea MSCI (EWY US)

- 2026 inflow surge: EWY has been the dominant Emerging Market flow story of 2026; Jan ($1.7bn), Feb ($2.8bn), and Mar ($1.5bn) saw record consecutive inflows, driven by the AI/semiconductor boom benefiting Samsung and SK Hynix.

- May 2026 reversal: A sharp ~$2.7bn outflow in May 2026, the largest single-month redemption in the period, as profit-taking took control after the extraordinary run-up.

- Recovery resuming: June and July 2026 month-to-date have seen strong inflows return (~$648m and ~$2.2bn respectively), consistent with this week’s five consecutive days of inflows.

The rotation away from China and into Korea within EM Asia allocations, driven by AI semiconductor tailwinds for Korea and persistent geopolitical/macro headwinds for China, remains in play, with fund managers appearing to use the recent weakness in the semiconductors to “get set”.

The Chinese economy continues to labour under a property collapse, lets hope were not next, while China’s economy remains weighed down by deflation, the prolonged property downturn and subdued consumer demand. Chinese exports have proven more resilient than expected despite US tariffs, but investor sentiment remains understandably cautious.

- We see no reason to buy the FXI ETF, but on balance we can see higher prices into 2027.