As we all know by now Credit Suisse has been bought by UBS in a deal orchestrated and backed by the Swiss Government. Equity holders will receive shares in UBS at a level 89% below where they were trading just 12 months ago, however, this is more than holders of Credit Suisse Hybrids (called ‘Cocos’ in Europe which stands for Contingent Convertible Capital Instruments) will receive – they get zero in the deal. i.e. Hybrid holders book a 100% loss. Securities that sit higher in the capital structure rarely get a worse outcome, however, there are some important aspects to note in this scenario:

- Government bailouts of high-risk European banks are common. In a government bailout scenario in Europe, hybrids must be written off to zero. This is not the case in Australia where they would be converted to equity in extreme circumstances.

- The CS Hybrids were very risky securities, carrying a very low credit rating, they were not listed, instead being traded in the Over-The-Counter (OTC) market which can be very grey – before the restructuring of CS, they were trading down ~70%.

- In the US/Europe, banks typically skip distributions and or treat first-call dates as truly optional. In Australia, if an Australian bank stops paying distributions on Hybrids, they cannot pay out dividends on the underlying shares, initiate buy-backs or even pay staff bonuses.

- Importantly, and this is the key, Australian banks are safe, incredibly well capitalised, and not involved in the business of risk that was obvious at Credit Suisse, while they are also traded on a transparent exchange which is not the case in Europe.

- The Market Matters Income Portfolio holds Hybrid securities, but these are limited to the highly rated, well-capitalised, and safe institutions of ANZ, CBA, NAB & WBC.

Now, let’s take a quick look at a couple of charts which illustrate what’s been unfolding in corporate bonds/hybrids both here and overseas posing the question, should we be scarred or looking for buying opportunities, two very different ends of the spectrum with plenty of shades of grey in between.

A comparison of the costs to hedge/protect debt exposure to the large Swiss banks and Australian names:

- Credit Suisse has been under increasing pressure for the last 6 months, its failure is not a classic “Black Swan” event.

- The cost of insuring against default by the Australian banks remains relatively low although it does not surprisingly edged higher this month.

chart

5-year Credit Default Swaps for Credit Suisse, UBS, CBA, and Macquarie Group

chart

5-year Credit Default Swaps for Credit Suisse, UBS, CBA, and Macquarie Group

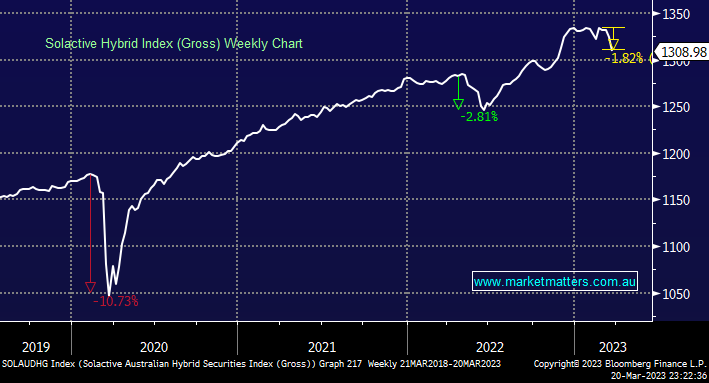

The Hybrid Index is down ~2% from the highs – nothing too sinister. The Average spread on ASX major bank 5-year hybrids has increased, moving from a very low 2.2% out to just under 3%. Yields on risker issuers like Macquarie & Challenger have moved out by more.

- MM believes the current weakness in Australian Hybrids is presenting better value for income-focused investors.

chart

Solactive Australian Hybrid Index (Gross)

chart

Solactive Australian Hybrid Index (Gross)