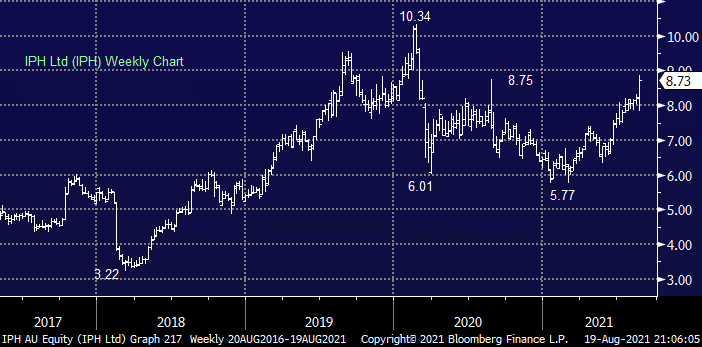

Intellectual property services company IPH rallied +5.6% yesterday making it the 7th best on ground after reporting FY21 earnings – the headlines were average with revenue down 2% to $363.5m and NPAT also 2% lower at $54.8m. However the company was able to deliver consistent earnings through the pandemic which is no mean feat, moving forward the board is focused on the combination of organic growth, consolidation of acquisitions plus increasing the use of its “network effect” with referrals in Asia up 25%.

Overall it looks likely the company will add to its 11 acquisitions since 2014, we like IPH moving forward believing its ~4.4% gross yield to be sustainable, an usual but potential candidate for our Active Income Portfolio.

MM likes IPH

Add To Hit List