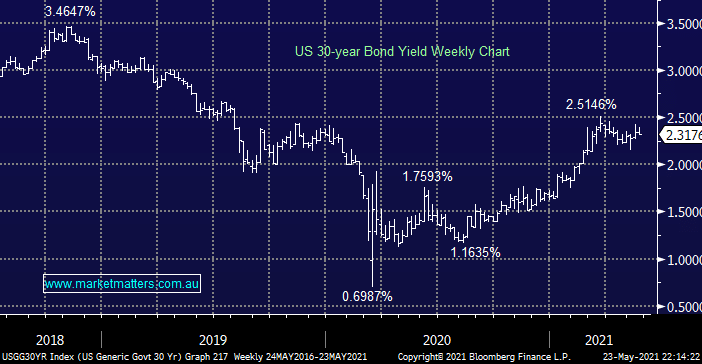

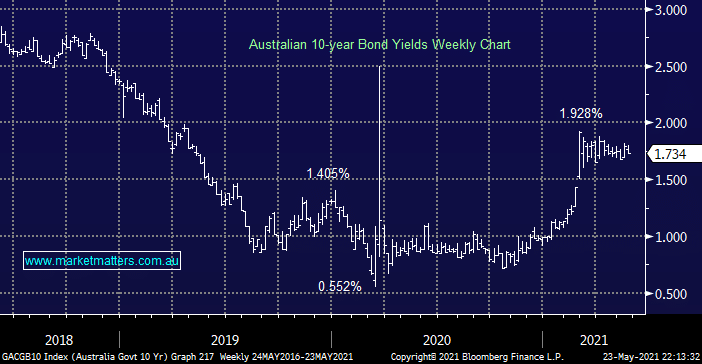

Bond markets have been trading sideways since late February, no great surprise considering the aggressive rally they experienced at the start of the year. We must remain 50-50 as to their direction short-term but we feel an attempt to test 2% will fail while a decline towards 1.5% represents great buying – at this stage considering the way bonds have reacted to recent news / economic data I feel they will probably test the downside first.

MM feels the next breakout in bonds is unlikely to follow through

The picture is very similar when we look at longer dated yields in the US where we are keen buyers of the 30-years around 2% but doubt they can break cleanly above 2.5% short-term however we believe they will be knocking on the door of 3-3.5% in 2022.