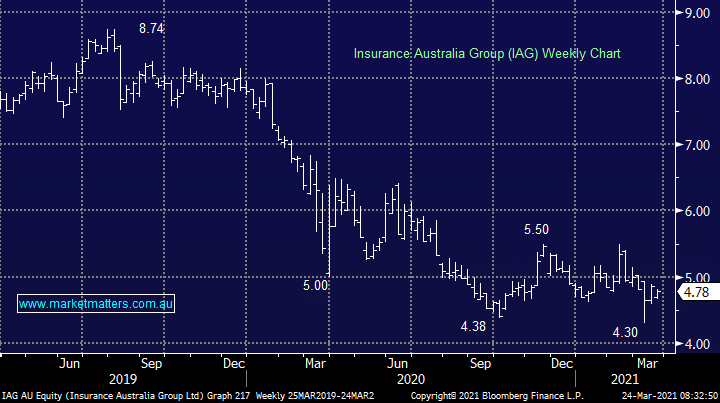

We added a new position to the portfolio last week namely the insurer IAG. This is a stock on the nose, it’s fallen from $8.80 this year to be trading just above its 52 week lows at $4.79 yesterday. We paid $4.69 for it with a 6% portfolio weighting. Putting the human element to the floods to one side, the actual financial hit to IAG is manageable. Macquarie say that their maximum loss is $169m given reinsurance however IAG were struggling before this anyway.

The market has been worried about their business insurance exposures during the pandemic however clearly the outcome here has been better than feared. It also seems to MM that the company is taking a very conservative approach around this and there is upside potential as a result, plus of course premiums will go up post floods and margins will expand.

IAG trades on an Est P/E of 19x FY21, however this is a year of recovery. Looking our to FY22, this number drops materially as underlying profit is expected to rebound, pushing that number closer to 15x, which is very cheap for IAG from a historical context. It’s also expected to yield 5.4% while we wait for the earnings recover.

MM are bullish IAG

Add To Hit List