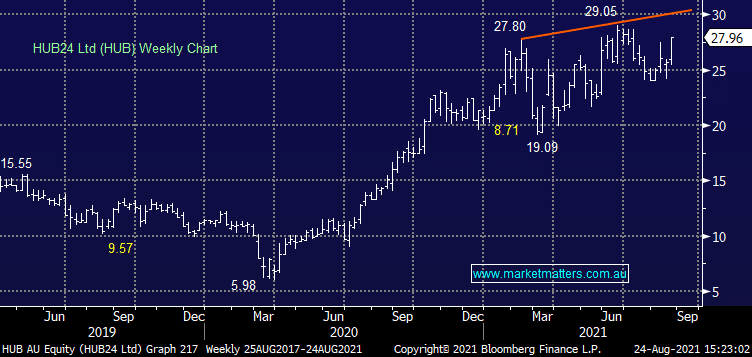

FY21 Results: HUB reported group revenue of $110.9m which is well below the $132m expected, Underlying EBITDA of $36.2m was a slight beat while underlying profit was largely inline. Key here is around FY23 Funds Under Administration (FUA) guidance which has been upgraded to a range of $63bn – $70bn by FY23, up from previous FY22 platform FUA guidance of $43bn – $49bn. This is a significant target considering our Analyst at Shaw James Bisinella’s current FY23 forecast was at $63.8bn and he’s traditionally above market. Margins the other key here with platform revenue margins of 34bps for 2H21 which is above main competitor Netwealth (NWL). We have HUB management in tomorrow for more flavour on the result, however this is growth company delivering on growth in FUA whilst also achieving decent margins. A good result and very understandable to see the stock trading 8% higher at time of writing.

MM remains long & bullish HUB

Add To Hit List