The ASX200 is a few days into what’s been a very quiet start to September, over the last decade August & September have combined to fall an average of -3.8% but last month’s +1.9% advance should have already warned statisticians that there’s nothing normal about the strength of the post COVID stock market rally – at MM we’re sticking with the trend of “Buy the dips but only fade the “pops” to new highs”. A quick comparison to the current rally with the one after the GFC illustrates the power of the current advance:

- In 2007/8 the ASX200 plunged 54% over 15-months as the GFC shook financial markets but it had only rallied ~60% after 5-years and it took over 12-years to break its pre-GFC high.

- Conversely during the initial COVID breakout the ASX200 plunged 38% in just 2-months but since its rallied over 70% in 18-months while taking only 15-months to break its pre-COVID high.

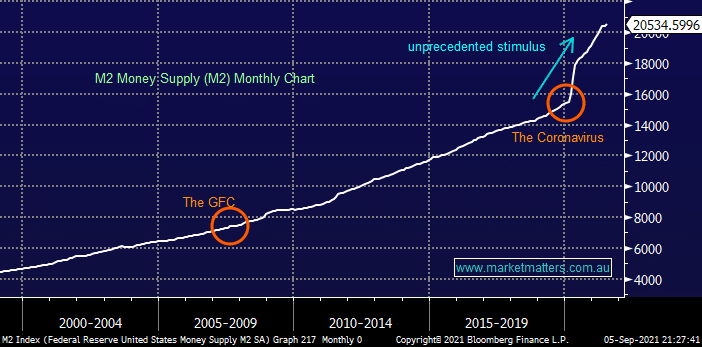

Clearly the recent market correction was much faster than in 2007/8 but the current recovery has eclipsed the one enjoyed over a decade ago in both magnitude and speed to recoup all of the losses, and post fresh all-time highs, as a guesstimate everything’s unfolding about 10x faster! With the risks around COVID clearly unlikely to vanish before we are well and truly into 2022, the unprecedented liquidity tailwind via both fiscal and monetary policy remains in play. The Fed & RBA might be discussing tapering their bond buying programs but they appear understandably concerned to stifle any economic recovery with another damaging COVID variant potentially lurking in the shadows.

Unprecedented liquidity / “free money” has driven asset prices through the roof including houses, art, cars and equities and while the US M2 Money Supply may have levelled off in 2021 as we’ve recently witnessed in NSW & Victoria governments aren’t going to be slow to press the stimulus button if / when outbreaks threaten economic recovery i.e. lockdowns.

NB M2 Money Supply measures the readily accessible cash & liquidity in society.