Most people think 2022 has been an awful year for equities but performance has actually been very stock/sector-specific, it hasn’t been an annulus horribilis for broad market investors. The ASX200 will commence its run towards Christmas this morning down less than 2% with dividends for the average portfolio more than making up for the slight fall. Last week we saw dovish comments from Fed Chair Jerome Powell weigh on bond yields and the $US which in turn ignited the interest rate-sensitive pockets of the stock market which could easily see the ASX close up for the year:

- “The time for moderating the pace of rate increases may come as soon as the December meeting” – Jerome Powell, Chair of the Fed Reserve.

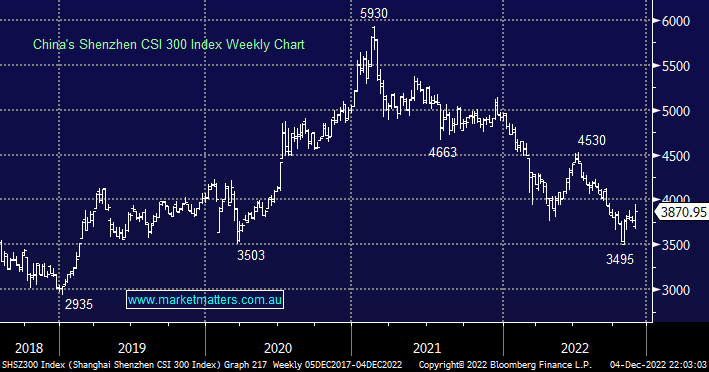

Over the weekend China added to the current positive tailwind for stocks as Beijing eased their aggressive Covid lockdowns which should improve the sentiment towards the already strong Resources Sector – the market will become more positive towards global economic growth. Elsewhere we can see investors scouring the landscape for the beneficiaries of China reopening their country:

- Shanghai residents will no longer need a 48-hour negative test to use public transport and enter outdoor venues – a large positive step by Xi Jinping et al.

This Tuesday at 2.30 pm the RBA will become the focus of investors’ attention, at least on our fair shores. MM believes that analysts and the market are being too pessimistic, we can see Phillip Lowe announcing no change with such a move likely to send local equities significantly higher.

- The market is factoring in a 77% chance that the RBA will hike another 0.25%, taking the cash rate to 3.1%, remember it started 2022 at just 0.1%.