While the awful humanitarian news continues to flow out of the Ukraine last week saw financial markets focus on the potential risks towards commodities markets and by definition global inflation if we see a prolonged conflict / economic stalemate. History tells us that higher inflation leads to rising interest rates which is a significant headwind for equities, and risk assets generally. Petrol prices have already gone crazy in Sydney, the local station has standard 95 at $2.35, I remember back in the middle of the Coronavirus panic it actually dipped under $1, that’s a clear read on inflation. We’ve all heard how commodity prices have exploded over recent weeks but its only just started to hurt our hip pockets – there’s a lot more to come!

If I’m noticing petrol prices you can guarantee the annoyance is far greater in the US, although Joe Biden doesn’t have to worry about Donald Trump until 2024 he wont be feeling comfortable about today’s fuel prices. The last time we saw oil prices trading as they have been through February & March was during the fuel crisis in the early 70’s which was the catalyst for a painful recession, exactly what the President wants to avoid. MM has no idea how successful the US will be but I have no doubt they are trying to replace Russian oil, and other commodities, from almost any source possible i.e. we wouldn’t be surprised to see a few rabbits pulled out of the proverbial hat over the coming weeks.

Hence MM believes the risk / reward has now switched firmly towards the downside for commodities over the coming weeks / months with last week already showing some cracks starting to form:

- Crude popped almost 20% last Monday but it ended the week down over 5%, falling more than 20% from its intra-week high.

- Coal might have made fresh 2022 highs last Monday, adding to the previous weeks 50% rally but it finally finished the 5-days down over 10%.

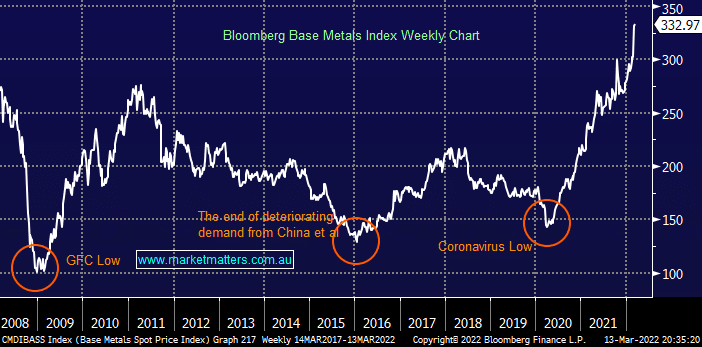

Base metals remained firm last week but after copper hit our long term target our preferred scenario is we see prices correct around 20% – not a major dent in the gains over the last 2-years.