- What Matters Today in Markets: Listen here each morning or find all Market Matters Podcasts on Spotify.

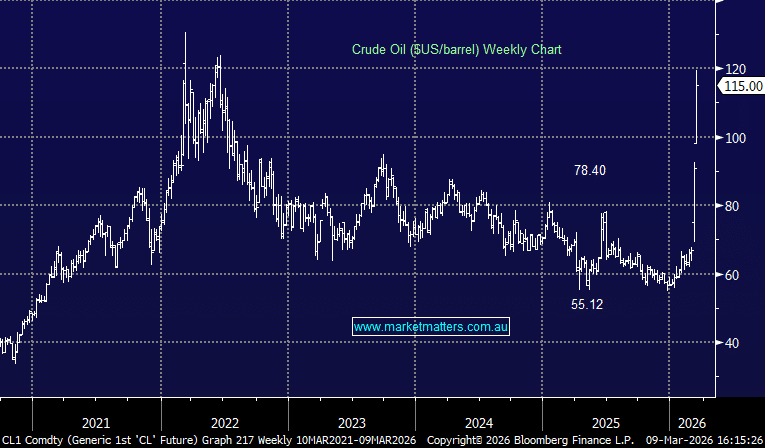

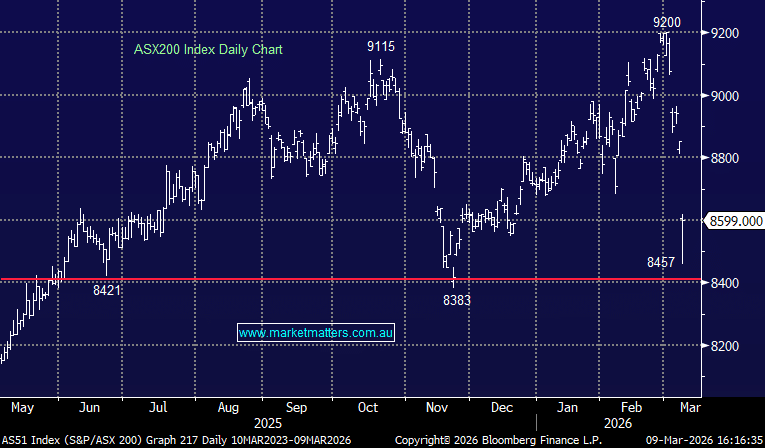

One week in, and the Iran war has already severely disrupted global energy markets, with threats to shipping through the Strait of Hormuz effectively choking oil exports from the Persian Gulf and pushing crude prices to their highest levels in more than two years. As producers cut output and energy prices surge, the conflict is raising global inflation risks and intensifying concerns about energy security, particularly in Europe. The local market initially shrugged off last weekend’s US–Israel strikes on Iran, with the ASX200 closing at an all-time high on Monday. However, that early optimism quickly faded as investors began to acknowledge the conflict could last far longer than first imagined:

- The ~28% surge in crude oil, pushing prices back above US$90/barrel, levels last seen when Russia invaded Ukraine, is weighing heavily on bond markets as the inflation outlook worsens by the day.

- At the same time, the outlook for global growth is weakening, with investors aggressively unwinding their once much-loved copper exposure.

Most of this can be gleaned from a quick read of almost any newspaper; the bigger question is what MM believes happens next, and how investors should position accordingly.

- Firstly, we remain bullish on equities through 2026, but this market pullback has not come as a surprise; it’s why we are carrying elevated cash positions across the MM Portfolios. Remember, in March/April 2025, we had a sharp pullback when President Tariff Trump released his tariff plans; in hindsight, this proved to be an excellent buying opportunity for cashed-up investors.

- Secondly, we remain very bullish on the AI & global electrification trade – meaning any pullbacks across semiconductors, copper and the broader energy complex we think should be viewed as buying opportunities, given the structural surge in electricity demand that lies ahead.

However, further volatility and weakness appear likely in the coming weeks as markets wait to see whether Trump has bitten off more than he can chew. The press is already drawing parallels with the Vietnam, Afghanistan and Iraq conflicts, where the US faced prolonged insurgencies and struggled to secure lasting political outcomes – but we doubt this will play out like these conflicts given how sensitive the current administration is to markets. Additionally, as we’ve mentioned a few times, the US President hasn’t got long to improve his flagging popularity with mid-terms in November providing a very good reason to wrap things up quickly.

- We are not political or commentators at MM, but the lower equities fall, the better the risk/reward becomes for investors.

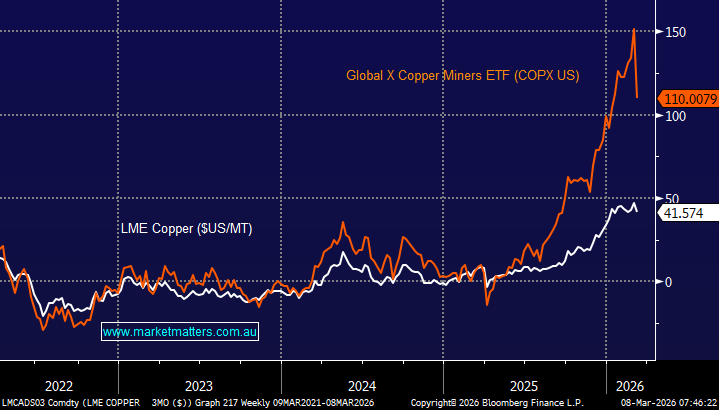

Copper was at the sharp end of investor selling last week as the physical market begins to soften. Sellers are increasingly struggling to move cargoes amid weaker demand, particularly in China, with inventories rising rapidly and Shanghai Futures Exchange stockpiles hitting record levels. At the same time, the “tariff trade” that previously drew large volumes of copper into the US is fading, sending excess supply back toward traditional markets in China and Europe. This has created a widening disconnect between physical fundamentals and futures prices.

While copper futures remain near record highs on speculative demand, the real-world market is starting to look oversupplied in the short term as buyers push back against elevated prices and manufacturers cut purchases. With global inventories climbing and some funds trimming bullish positions, the key question is how long prices can remain elevated if underlying demand continues to weaken.

However, in our opinion the real disconnect had occurred in copper stocks which had significantly outperformed the industrial metal acknowledged by most investors as critical for global electrification. We shouldn’t forget last month’s Bank of America Fund Managers Survey, which again identified long gold and commodities as two of the most crowded positions in the market – in other words, the market was ripe for some profit-taking.

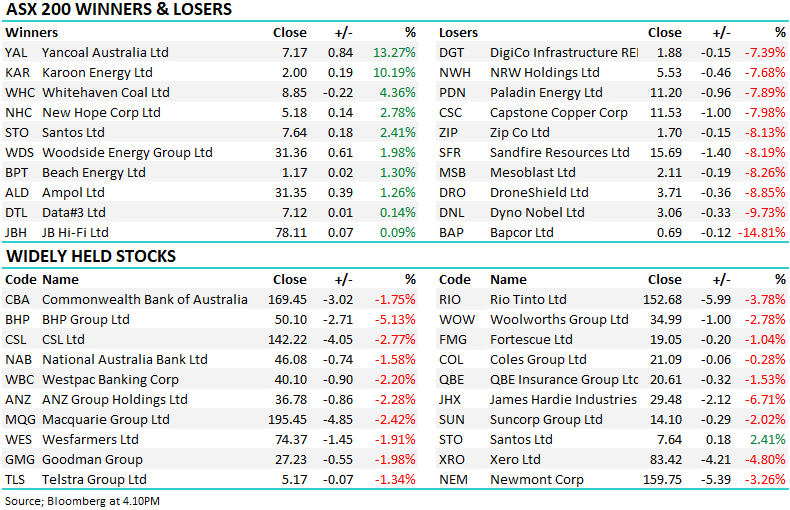

- In the last few weeks, copper has slipped ~5%, but the copper names have been slammed, e.g. Freeport McMoRan (FCX US) -15%, Sandfire (SFR) -18%, and Capstone Copper (CSC) -27%.

We can see another 10-15% downside in the sector, but we already believe the sector is closer to being a buy than a sell.