- What Matters Today in Markets: Listen here each morning or find all Market Matters Podcasts on Spotify.

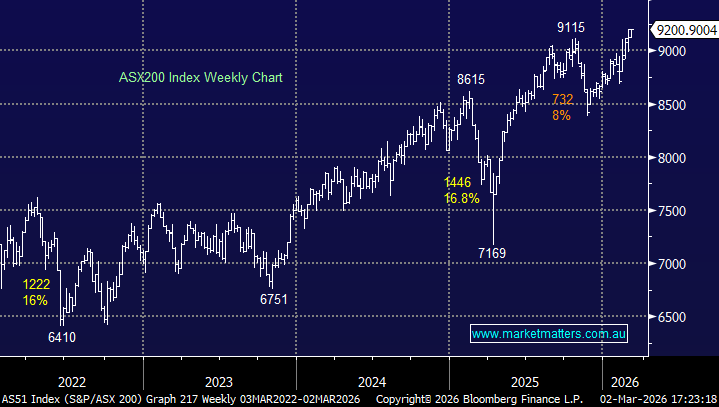

The ASX200 was firm on Monday, shrugging off the conflict in the Middle East to close marginally higher, trading and closing above 9200 for the first time – not a good day for the bears! The index clawed back early losses as heavyweight miners rebounded from initial weakness to push firmly into positive territory. BHP led from the front, rallying over $2 from its early low to end the session up +1.4% at another all-time high, adding 14-points to the index on its own. By the close, the Materials and Energy Sector combined to add 67-points to the main board, offsetting the 55-point negative contribution from the financials as the story remained the same on the performance front.

Volatility was most noticeable in the likes of precious metals and oil which were reacting directly towards the continuous news flow around Iran:

- During our trading session, gold traded in more than a $U100/oz range, almost following silver into negative territory around midday AEST.

- Oil was strong as expected, spending most of our day session up ~7%, although at one stage it was up over 10%.

The moves were generally controlled with markets listening to President Trump’s message that the bombing could last several weeks, but the underlying belief appeared to be that the US and Israel would ultimately prove successful. Two major concerns emerged following the weekend attacks, though one now appears to be largely off the table.

- Iran’s bombing of its neighbours, including Iraq, Kuwait, Bahrain, Qatar, UAE, and Oman, disrupting key aviation hubs and oil shipments, will likely leave Iran isolated across the region during the conflict with the US and Israel.

- The conflict has effectively shut the Strait of Hormuz, a vital artery off Iran’s coast that carries about a fifth of the world’s oil and significant volumes of gas – if this remains closed for a prolonged time, it’s going to hurt financial markets.

At MM, we believe that Israel and the US will ultimately triumph because they simply need to and have the military might at their disposal. With Trump’s midterms looming in November, this must be a swift victory; otherwise, it’s likely to become a political drag. Hence, “our best guess” is that the conflict will escalate further but end within Trump’s “4 weeks”.

- The markets agreed last night, with gold and oil surrendering most of their initial gains to end the session up only 0.9% and 2.5% respectively, while silver was down close to 5%.

Overseas indices were mixed, although many markets didn’t see the late recovery in the US. In Europe, the German DAX fell 2.6% and the UK FTSE 1.2%. Conversely, in the US, the NASDAQ gained +0.1% and the small-cap Russell 2000 0.9% as tech dip-buying surfaced when the major indices traded down towards their 2026 lows.

- The SPI Futures are calling the ASX200 to slip 0.2% this morning, with some profit-taking likely in the resources sector.