The ASX200 rallied another +2.1% last week, posting a fresh closing high on Friday, extending July’s gain to +2.5%. Gains were broad-based over the five days, with all 11 of the main sectors closing higher, led by Tech and healthcare, which surged +5.2% and +4.8% respectively. The trend remains clearly bullish, and while the average gain for the month of July over the last decade is around 3% equities are breaking to new highs with strong momentum, and as we mentioned on Friday morning, the surprises in markets usually unfold with the trend – the best two Julys of the last decade have delivered gains closer to 6%.

- The market’s current strength was demonstrated by the way it shrugged off rising long-term bond yields, something that’s caused corrections in the past.

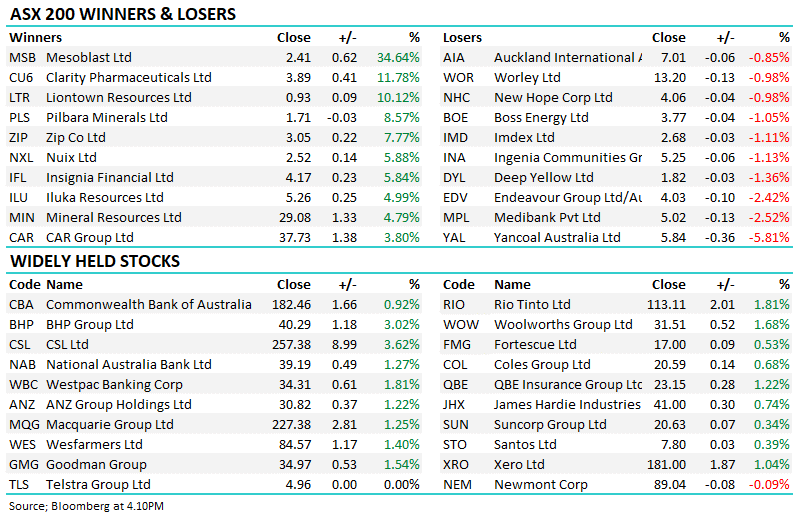

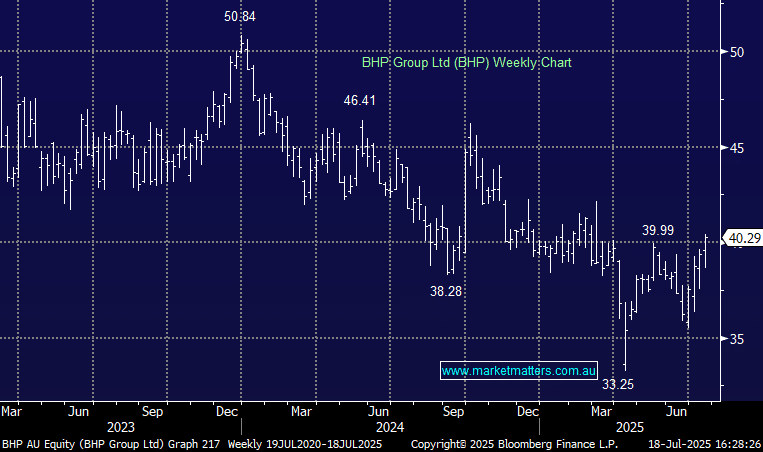

While plenty of stocks rallied 5% or more, the real backbone of last week’s stellar performance was the combination of gains by the heavyweight stocks: CSL Ltd (CSL) +6.8%, BHP Group (BHP) +2.4%, and an average advance of 0.9% by the “Big Four Banks.” Again, we saw the underperformers of the last 12-18 months outperform as stock and sector rotation was ongoing, with investors seeking some semblance of value in the market, pushing towards 8800.

By the close on Friday, the winners and losers enclosure saw a diverse bunch of names leading the way, while only around 15% of the ASX200 retreated for the week:

Winners: Life360 (360) +14.9%, Paladin Energy (PDN) +12.8%, HUB24 (HUB) +11.5%, Macquarie Tech (MAQ) +11%, PolyNovo (PNV) +10.5%, Pilbara (PLS) +10.3%, Pinnacle (PNI) +9.2%, Generation Dev. (GDG) +8.8%, DigiCo (DGT) +8.4%, and CSL Ltd (CSL) +6.8%.

Losers: South32 (S32) -7.1%, Yancoal (YAL) -6.1%, James Hardie (JHX) -4.4%, Alcoa (AAI) -3.2%, Endeavour Group (EDV) -2.7%, Genesis Materials (GMD) -2.2%, Super Retail (SUL) -2%, Sigma Healthcare (SIG) -1.8%, and Newmont (NEM) -1.6%.

On the economic and geopolitical front, the market refocused on good old-fashioned earnings while talk around tariffs was relatively muted:

- On Wednesday, Chinese growth data came in better than expected, helping iron ore recover back above $US100/MT.

- Bloomberg reported that Federal Reserve Governor Christopher Waller said US interest rates should be cut before the labour market shows further signs of deterioration; markets are pricing in two cuts by the FED in the next six months.

- Soft Australian employment data on Thursday brought three rate cuts this side of Christmas back into play, creating a tailwind for the markets’ explosive move on Friday; markets are pricing in a “probable” three cuts by the RBA in the next six months.

- On Thursday night, US retail sales saw a broad advance in June, tempering concerns about a pullback in consumer spending and lifting confidence in the US economy.

- On Friday night, stocks had a more muted session on concerns Trump was pushing for 10-15% tarrifs accross the board as a base line, and higher in some instance, but it still wasn’t enough to push any major indices down by more than 0.5%.

- Overall equities remain well supported, helped by 12% of S&P 500 companies which have reported results, 83% have beaten estimates, and as we often say, earnings ultimately drive stocks.

Overseas markets drifted lower into the weekend after President Trump reportedly pushed for greater tariffs on the EU. According to the Financial Times, Trump is demanding a minimum tariff of between 15% and 20% in any deal, which sent European bourses lower. The EURO STOXX 50 and German DAX both slipped 0.3% while the UK FTSE managed to eke out a 0.2% gain. In the US, the S&P 500 and tech-based NASDAQ both slipped less than 0.1%.

- The SPI Futures are calling the ASX200 to open down 0.6% on Monday we enjoyed strong outperformance on Friday.