Over recent weeks we’ve looked at a number of software companies that have fallen well out of favour with investors despite maintaining solid underlying businesses. Fineos (FCL) sits firmly in that camp.

The Irish-based software provider, which specialises in core administration systems for life, accident and health insurers, has endured a difficult few years. Once viewed as a premium software growth story, the stock has gradually de-rated as growth slowed, implementation cycles lengthened and investor enthusiasm for smaller enterprise software names evaporated.

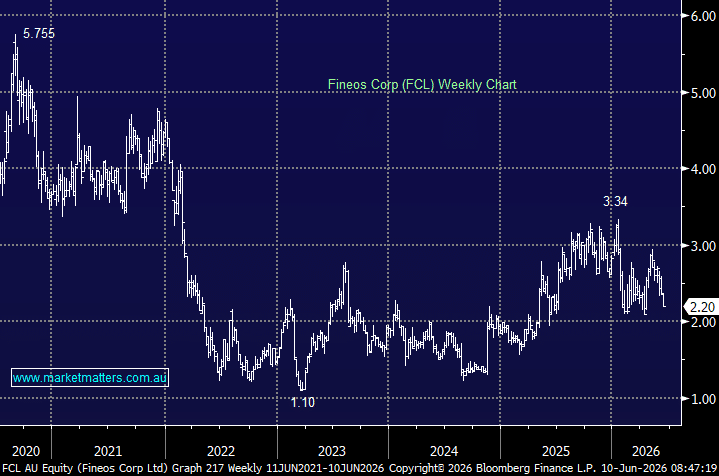

- The result is a stock trading more than 70% below its post-COVID highs despite the business itself continuing to make progress.

What makes Fineos interesting today is that the market appears to be pricing it as though growth has largely disappeared, yet the company remains well positioned within a niche market where it enjoys strong competitive advantages and high customer switching costs.

Unlike many software businesses targeting small and medium enterprises, Fineos sells mission-critical systems to large insurance providers. These are not products customers can easily replace. Once embedded within an insurer’s operations, the software becomes deeply integrated into claims management, policy administration and customer servicing functions. That creates sticky revenue streams and long-term customer relationships.

- The challenge has been translating that position into the sort of growth investors expected when software valuations were at their peak.

Over recent years management has deliberately shifted the business towards a cloud-based subscription model. While strategically the right move, transitions of this nature often create a period where reported revenue growth appears less impressive than the underlying operational progress. Investors have become impatient waiting for the benefits of the transition to fully emerge.

At the same time, enterprise software spending globally has become more scrutinised. Large customers are taking longer to approve projects and implementation timelines have stretched. Fineos has not been immune to those industry-wide headwinds, and the stock has been whacked.

However, unlike many speculative software businesses that have struggled in the higher interest rate environment, Fineos has already demonstrated an ability to generate positive cash flow and improve profitability. This is not a distant growth story, but a company becoming financially self-sufficient.

The software sector remains one of the most polarised areas of the market, however, we believe the tide is starting to turn. While investors continue to reward companies directly exposed to AI themes, they are largely ignoring many traditional enterprise software businesses. As a result, valuation dispersion across the sector has become extreme.

- The company is not an AI beneficiary. It operates within a specialised insurance vertical that rarely captures investor attention. Yet these are often the characteristics that create opportunity when sentiment becomes overly pessimistic – as we think it is today.

Importantly, Fineos still has a substantial growth runway. The global life, accident and health insurance market remains highly fragmented from a technology perspective, with many providers operating on legacy systems that are increasingly expensive to maintain and difficult to modernise. Fineos continues to benefit from this long-term digitisation trend.

The question for investors is not whether the company has a market opportunity. It clearly does. The question is whether management can consistently convert that opportunity into accelerating revenue growth and expanding margins.

For us, Fineos shares some similarities with other beaten-up software names we’ve discussed recently. The valuation has compressed significantly, expectations have been reset lower and investor positioning is particularly negative. Those conditions often provide fertile ground for positive surprises if operational performance begins to improve.

- The risk is that growth remains subdued for longer than expected. Enterprise software recoveries take time, and investors may need to remain patient.

However, at current levels, Fineos no longer needs to deliver perfection. The market has already substantially lowered its expectations. If management can continue improving profitability while demonstrating that growth remains intact, there is scope for sentiment to improve materially from here.

As we’ve noted with several software stocks recently, the opportunity often emerges when investors stop focusing on what a company was expected to become and start assessing what it actually is today.

While we are not suggesting Fineos deserves to trade anywhere near the multiples seen during the software boom, we do think the stock now warrants a place on our Hitlist – for further monitoring. The business remains strategically well positioned, the balance sheet is sound, and expectations have become sufficiently low that execution rather than market enthusiasm is likely to drive returns from here.

MM is adding FCL back onto the Emerging Companies Hitlist ~$2.20

Add To Hit List