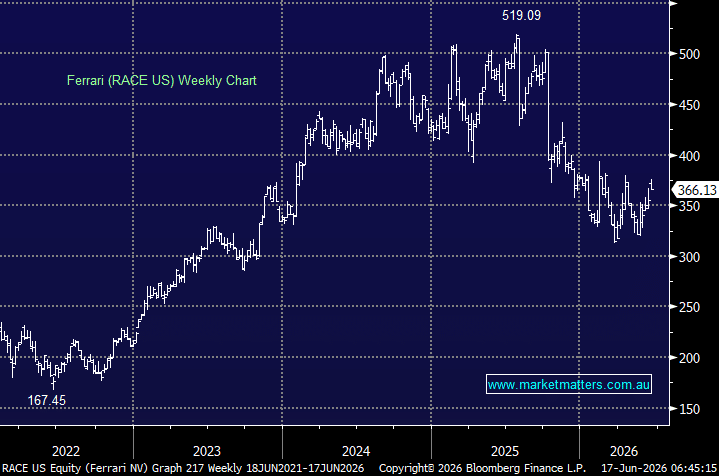

Ferrari shares have come under pressure following the unveiling of the Luce, its first fully electric vehicle, with investors questioning whether the design represents a step too far from the performance, sound and heritage that underpin the brand.

chart

New Ferrari Luce (EV) – Source: thebeep.com.au

chart

New Ferrari Luce (EV) – Source: thebeep.com.au

The initial reaction was undeniably poor. The shares fell around 6% following the presentation as criticism focused on the car’s unconventional design, five-seat configuration and starting price of approximately €550,000. For a company whose valuation rests heavily on scarcity and brand equity, anything suggesting potential dilution of the Ferrari identity will naturally attract scrutiny.

However, we think the market may be reading too much into one vehicle. The Luce is better viewed as an extension of Ferrari’s range rather than a wholesale repositioning of the brand.

Internal-combustion and hybrid vehicles will remain central to Ferrari’s product mix and profitability for the foreseeable future. The company is not abandoning its traditional customer; it is offering an additional model aimed partly at existing owners who already have an EV in the garage, as well as prospective buyers considering electric models from competing luxury brands.

We read an interesting note from UBS following discussions with more than 15 Ferrari customers, which indicated that underlying loyalty remained stable, despite muted enthusiasm for the Luce itself. UBS also believes the controversial design is more likely to be a one-off than a signal of Ferrari’s future design direction.

Importantly, the economics appear sound. While the vehicle’s pricing has attracted criticism, margins are tipped to be broadly consistent with Ferrari’s other range models, with a typical four-to-five-year lifecycle. In other words, the Luce does not need to redefine Ferrari to be commercially successful.

The broader business also remains in excellent shape. On consensus forecasts, revenue is tipped to increase from €7.5 billion in 2026 to €9 billion by 2029, while EBITDA rises from around €3 billion to €3.6 billion. Margins are also forecast to expand, with return on invested capital moving above 40% and the balance sheet trending toward a net-cash position.

Following the pullback, Ferrari trades at around 32x forecast 2026 earnings and 29x 2027 earnings. That remains a premium valuation, but it is materially below the multiples investors have regularly paid for the stock (~40x) and increasingly compares Ferrari with the world’s leading luxury houses rather than conventional car manufacturers. UBS retains a Buy rating and a US$483 price target.

The weekend also provided a timely reminder of the power of Ferrari’s racing heritage, with Lewis Hamilton claiming his first Grand Prix victory for the Scuderia in Barcelona. Formula One success does not drive near-term earnings, but it remains an important part of Ferrari’s global appeal, exclusivity and emotional connection with customers.

- We share UBS’s optimism. The Luce may not appeal to every Ferrari enthusiast, but one divisive model does not undermine a business built on scarcity, pricing power, long waiting lists and one of the world’s most valuable brands.

MM is bullish RACE ~$US360

Add To Hit List