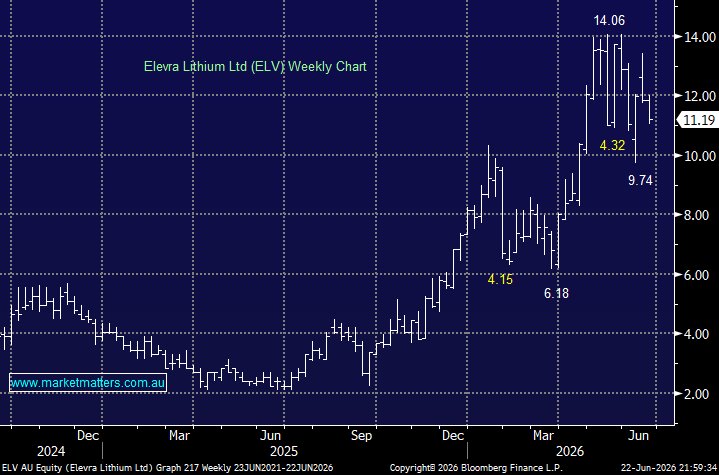

Elevra Lithium was formerly known as Sayona Mining Limited, rebranding in August 2025. It’s a $2.2bn North American lithium producer dual-listed on the ASX and in the US (NASDAQ: ELVR), with projects in Québec, Canada, the United States, and Western Australia. Like a number of its peers, it was dropped from the ASX200 in March 2024 as the lithium price collapsed – a great example of the trials and tribulations of a cyclical miner.

Elevra is on target to deliver ~$257mn revenue and turn a profit in FY26, but obviously, that’s highly correlated to the lithium price. In the March quarter, ELV delivered record revenue of US$81m (+22% QoQ), generated an operating profit of US$32m and finished the period with a net cash position of US$58.7m – their June quarter numbers are set to drop in the coming weeks. If the lithium price remains firm, ELV is an exciting “cash cow” with the company, largely through its major restart investment phase, meaning improving lithium prices should increasingly translate into cash flow and balance sheet strength rather than being absorbed by significant capital expenditure.

Lithium prices have fallen sharply over the last 48-hours as speculation emerged that CATL’s Jianxiawo lithium mine in China could restart later this year. While no formal restart has been confirmed, the prospect of additional supply was enough to weigh on an already fragile market. This shouldn’t come as a major surprise with mothballed mines eyeing off improving lithium prices.

- At this stage, we see good risk/reward towards ELV ~$10.