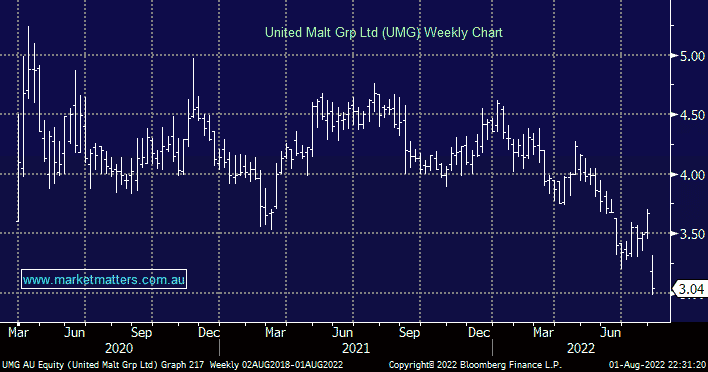

Yesterday we saw commercial malt business UMG, which was previously demerged from GrainCorp (GNC), tumble over -17% to fresh all-time lows following a major earnings downgrade. They’re now targeting a top-end EBITDA of $108mn, over 22% below their previous top-end $140mn guidance. The company has struggled with poor quality / high-cost North American barley which is flowing down into higher production costs and falling margins, never a good combination – beer prices that look set to rise are a major concern! The business is optimistic about an improvement in H2 but hope doesn’t pay the bills!

- We aren’t keen on UMG which has shown it cannot control its own destiny while the company’s shares aren’t cheap enough to offset these clear risks to profitability.

MM is neutral/negative UMG around $3

Add To Hit List