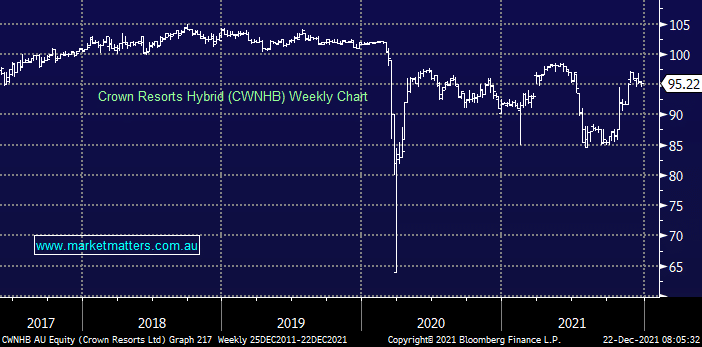

These higher risk hybrid securities are trading at $95.22 and pay a running yield of 4.24%, the ‘fat’ will come from redemption at $100 face value. If that happens in 12 months, the return will be the yield + the 4.75% capital growth equalling~9%. If they take two years to redeem them, the capital gain will be halved and the annual return will be ~6.6% and so forth. We think CWN will ultimately be sold, if it’s to Blackstone, they can source debt a lot cheaper than what the hybrids cost, and the same is probably true for other suitors. If the bids are pulled and Crown goes it alone, they have a significant amount of property sales to settle over the coming year which would see them pay down debt, starting with the hybrids. While the risk is they leave these outstanding indefinitely, we think that scenario is a very low probability.

MM is a happy buyer of CWNHB ~$95.22

Add To Hit List