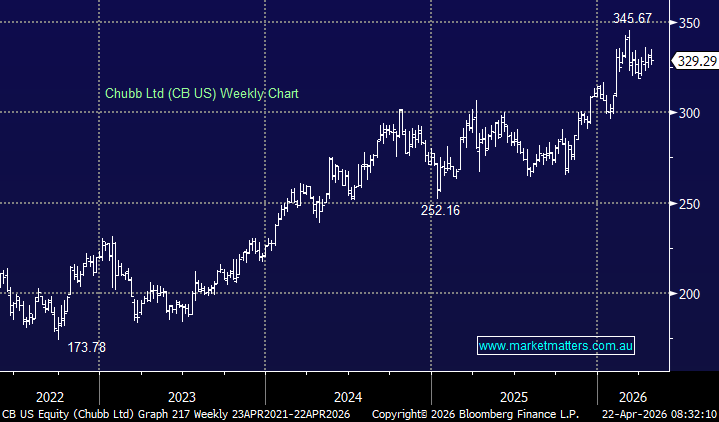

Chubb delivered a strong March quarter result this morning, reinforcing why we continue to like the stock. Core operating earnings came in ~3% ahead of expectations, while net premiums written rose 10.7% to $US14.0bn. Investment income was also a standout, highlighting the benefit of Chubb’s scale, balance sheet strength and disciplined portfolio construction.

1Q result highlights:

- Net premiums written $US14.01 billion, +11% y/y, estimate $US13.49 billion

- Core operating EPS $US6.82 vs. $US3.68 y/y, estimate $US6.60

- Net premiums earned $US13.46 billion, +12% y/y, estimate $US13.28 billion

- Core operating ROE 14% vs. 8.6% y/y, estimate 13.6%

- Property & casualty combined ratio 84% vs. 95.7% y/y, estimate 85%

- Loss and loss expense ratio 55.6% vs. 67.8% y/y, estimate 57.3%

- Total investments $170.20 billion, +0.9% q/q

The headline earnings growth was flattered by a much lower catastrophe burden than the prior corresponding period, which had been hit by the California wildfires, but the underlying result was strong regardless. Ex-CATs, core operating income rose 10.7% and EPS increased 13.5%, while current accident year underwriting income excluding catastrophe losses grew 9.8%, with a very strong combined ratio of 82.1%. In other words, it was another quarter of high-quality execution.

Chubb is a genuinely diversified global insurer with meaningful exposure across commercial P&C, consumer insurance and life, and the geographic mix again mattered in the quarter. North America P&C net premiums written rose 4.1%, while Overseas General grew 14.4%, with particularly strong contributions from Latin America, Europe and Asia. Life premiums were even stronger, up 33.1%, underscoring Chubb’s diversification – it is far more than a one-dimensional insurer leveraged to a single market or cycle.

Importantly, management also showed the sort of underwriting discipline we want to see from an insurer we own. CEO Evan Greenberg called out that parts of the property and financial lines market are softening, with sections of property softening rapidly, and Chubb responded by reducing exposure in areas where pricing had become inadequate while buying additional reinsurance.

This is important from a risk perspective. Chubb has never been about chasing premium growth at any cost; it is about writing profitable business, protecting returns and compounding book value over time.

Chubb remains a growth-at-a-reasonable-price name: a very well-run global insurer, with broad diversification, underwriting discipline, growing investment income, strong returns on equity and a management team that has repeatedly shown it knows when to press and when to pull back. In a more uncertain macro backdrop, these attributes are particularly important, and this result was another example of solid execution.

- From a valuation perspective, CB trades on an Est PE of 12x, growing underlying earnings at 5-6% YoY. The result was very solid, though that was not unexpected. We don’t expect any meaningful share price reaction to the numbers.